Data Governance, Decision Discipline, and Competitive Foresight in Two Distinct Markets

Research Publication by Temitope Sule-Akinsemoyin

New York Center for Advanced Research (NYCAR)

Institutional Review

June 2026

DOI: https://doi.org/10.5281/zenodo.20627986

Publication Number: NYCAR-TTR-2026-RP056

Peer Review Status: Approved for publication release. This doctoral research publication meets the New York Center for Advanced Research (NYCAR) standard for advanced strategic-management scholarship, source discipline, APA 7th accuracy, comparative case analysis, and professional presentation. The paper demonstrates strong command of strategic business intelligence as an executive discipline, with practical attention to data governance, decision quality, corporate foresight, analytics maturity, AI risk, and organizational accountability. Its Australia and Georgia case orientation gives the study comparative value by showing how business intelligence changes when institutions differ in market scale, digital maturity, and governance capacity. The work is approved as a complete doctoral research publication suitable for institutional, academic, and professional readership without appendix material.

Abstract

This doctoral research publication studies strategic business intelligence in the corporate world with case studies from Australia and GeorgiAIn corporate environments in Australia and Georgia where digital maturity, analytics, and decision governance shape competitiveness. The work is deliberately applied: it uses current public evidence, institutional cases, and conceptual analysis to build a practical argument for leaders who must make difficult decisions under constraint. The central claim is that modern institutions cannot rely on inherited forms when public trust, technology, cost pressure, learner or customer expectations, and social inequality are changing the meaning of performance. The publication develops a conceptual model, comparative case analysis, diagnostic tools, black-and-white figures, and implementation tables. It treats data as evidence, not decoration, and treats theory as a tool for disciplined judgment rather than academic display. The final position is that serious institutional renewal requires proof: visible routines, accountable governance, ethically defensible choices, and a readiness to correct weak systems before they become public failure.

Keywords: strategic; business; intelligence; corporate; advantage; lessons; australia; georgia; NYCAR; applied research; governance; policy; institutional reform

Contents

Introduction: Business Intelligence as Executive Discipline

Strategic BI Foundations and Corporate Decision Quality

Australia: Analytics, AI Investment, and Data Governance

Georgia: Digital Transformation, Enterprise ICT, and Market modernization

Corporate Case Studies in Banking, Retail, Logistics, and Public-Private Systems

Data Quality, Dashboards, and the Politics of Measurement

AI, Predictive Analytics, Cyber Risk, and Ethical Intelligence

Strategic BI Formula and Comparative Readiness Model

Implementation Blueprint for Australia and Georgia-Informed Corporations

Final Position: Intelligence That Changes Decisions

List of Tables and Figures

Table 1. Australia and Georgia corporate BI comparison

Table 2. Strategic BI decision protocol

Table 3. BI risk register

Figure 1. Australia-Georgia digital readiness comparison.

Figure 2. Strategic BI capability mix.

Figure 3. Georgia enterprise ICT adoption signals.

Figure 4. Australia corporate BI use cases.

Figure 5. BI decision quality controls.

Figure 6. Business intelligence maturity curve.

Figure 7. BI risk exposure.

Figure 8. Implementation priorities.

Chapter 1: Introduction: Business Intelligence as Executive Discipline

1.1 The executive problem behind business intelligence

The gap between executive appetite for intelligence and the discipline required to use it well cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For executive discipline, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through executive discipline: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

1.2 Australia-Georgia evidence and executive context

The section on australia-georgia evidence and executive context places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for australia-georgia evidence and executive context needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under australia-georgia evidence and executive context, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for australia-georgia evidence and executive context is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

1.3 Management decisions that give data authority

Management choices around the gap between executive appetite for intelligence and the discipline required to use it well begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of executive discipline, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for executive discipline links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

1.4 Early risks in data-led corporate strategy

The section on early risks in data-led corporate strategy places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for early risks in data-led corporate strategy needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under early risks in data-led corporate strategy, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for early risks in data-led corporate strategy is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

1.5 Learning routines that make intelligence durable

Institutional learning is the part of the gap between executive appetite for intelligence and the discipline required to use it well that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in executive discipline also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for executive discipline is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

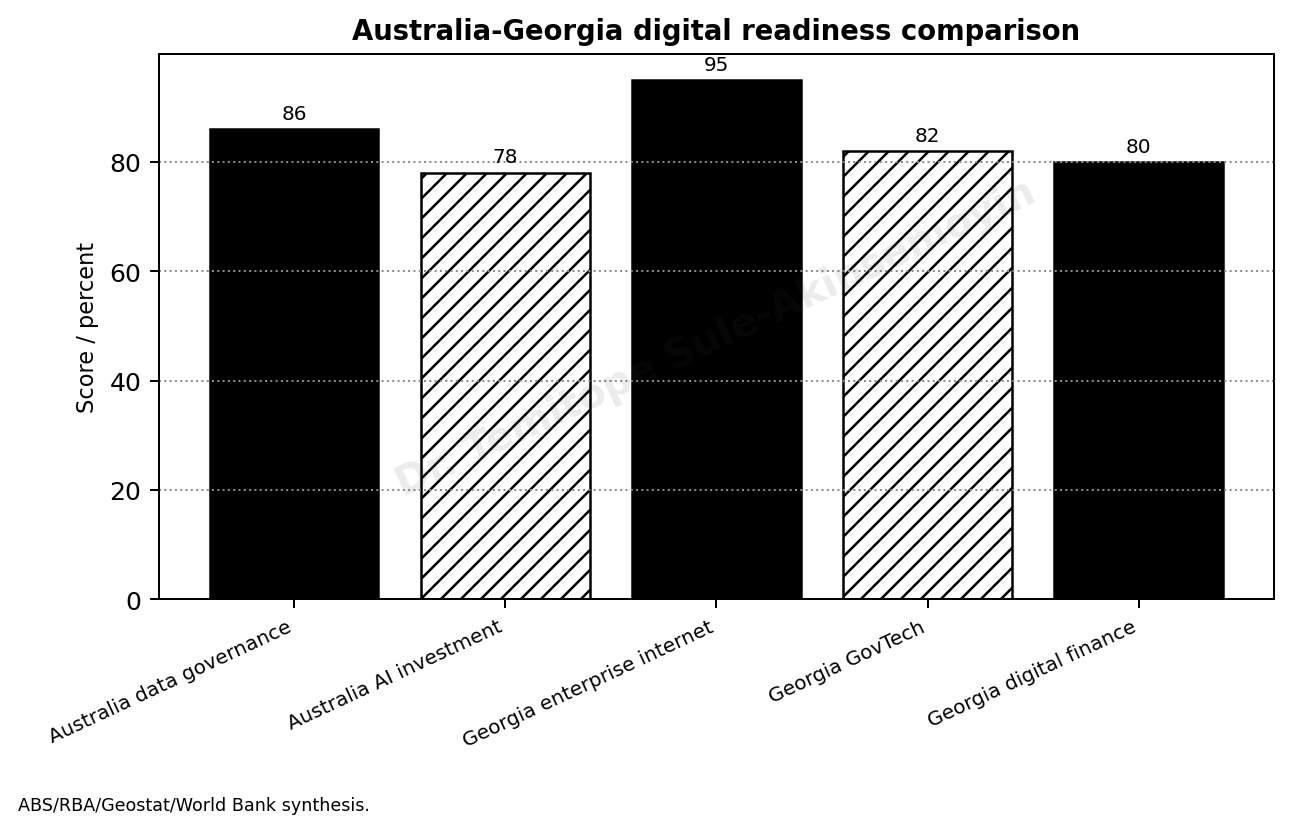

Figure 1. Australia-Georgia digital readiness comparison.

Source: ABS/RBA/Geostat/World Bank synthesis.

Chapter 2: Strategic BI Foundations and Corporate Decision Quality

2.1 From reporting culture to decision discipline

The movement from reporting culture to corporate decision quality cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For decision quality, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through decision quality: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

2.2 Evidence on decision quality and reporting limits

The section on evidence on decision quality and reporting limits places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for evidence on decision quality and reporting limits needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under evidence on decision quality and reporting limits, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for evidence on decision quality and reporting limits is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

2.3 Ownership of data, judgment, and accountability

Management choices around the movement from reporting culture to corporate decision quality begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of decision quality, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for decision quality links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

2.4 Risks when measurement replaces judgment

The section on risks when measurement replaces judgment places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for risks when measurement replaces judgment needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under risks when measurement replaces judgment, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

Pace matters when business intelligence moves from dashboard talk to corporate decision-making. Early work should concentrate on data ownership, decision rights, reporting discipline, staff confidence, and the correction of errors already visible to managers. A company gains more from a tested reporting routine than from a larger analytics platform that leaders do not trust.

2.5 Building a BI culture that survives leadership change

Institutional learning is the part of the movement from reporting culture to corporate decision quality that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in decision quality also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for decision quality is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

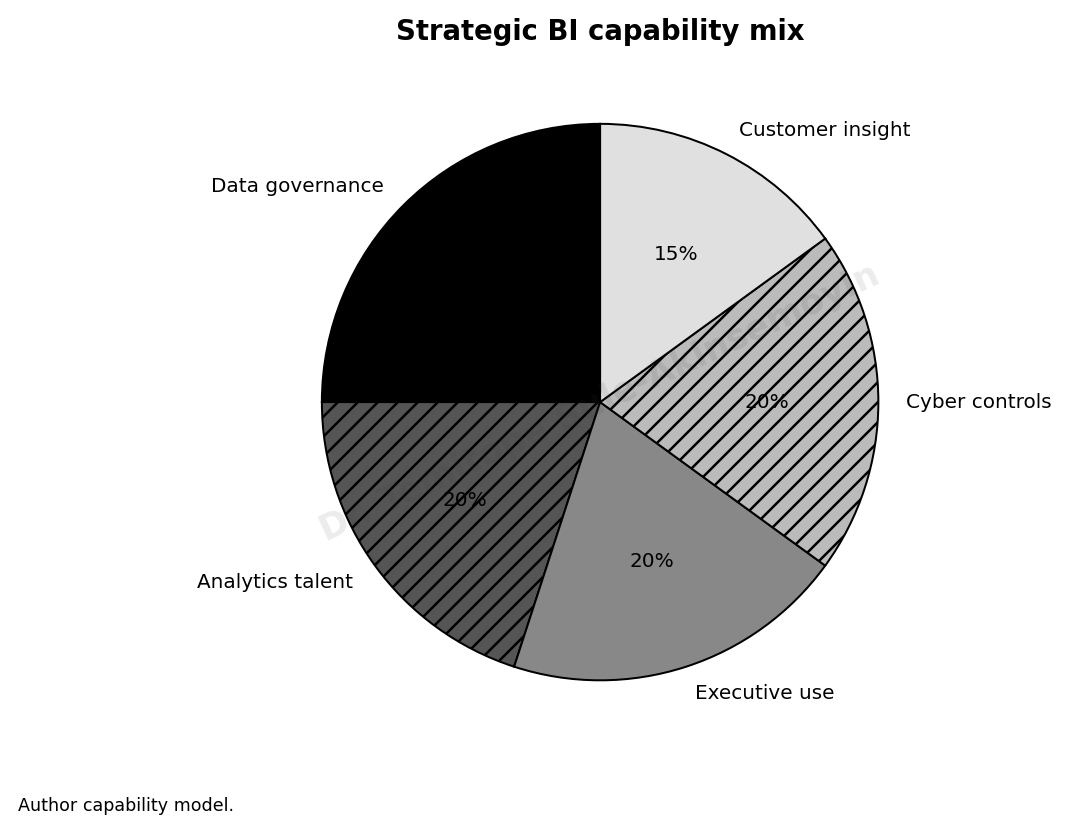

Figure 2. Strategic BI capability mix.

Source: Author capability model.

Chapter 3: Australia: Analytics, AI Investment, and Data Governance

3.1 Australia’s analytics advantage and its limits

Australia’s mature analytics environment, ai investment, and data-governance pressure cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For Australian analytics and AI investment, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through Australian analytics and AI investment: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

3.2 Australian evidence on AI, regulation, and analytics

The section on australian evidence on ai, regulation, and analytics places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for australian evidence on ai, regulation, and analytics needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under australian evidence on ai, regulation, and analytics, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for australian evidence on ai, regulation, and analytics is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

3.3 Data governance in banks, services, and public systems

Management choices around Australia’s mature analytics environment, AI investment, and data-governance pressure begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of Australian analytics and AI investment, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for Australian analytics and AI investment links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

3.4 Australian risks in privacy, automation, and scale

The section on australian risks in privacy, automation, and scale places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for australian risks in privacy, automation, and scale needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under australian risks in privacy, automation, and scale, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for australian risks in privacy, automation, and scale is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

3.5 Lessons for firms working in mature digital markets

Institutional learning is the part of Australia’s mature analytics environment, AI investment, and data-governance pressure that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in Australian analytics and AI investment also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for Australian analytics and AI investment is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

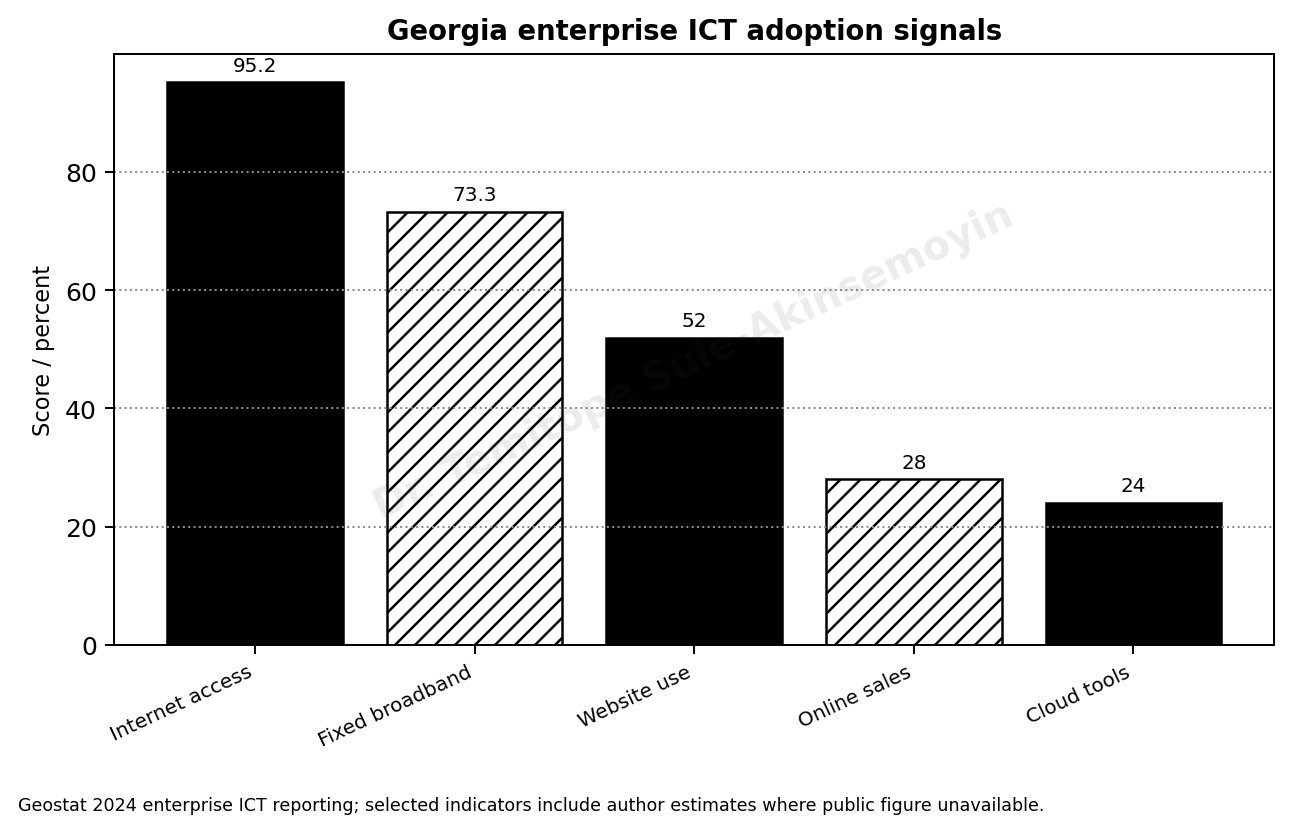

Figure 3. Georgia enterprise ICT adoption signals.

Source: Geostat 2024 enterprise ICT reporting; selected indicators include author estimates where public figure unavailable.

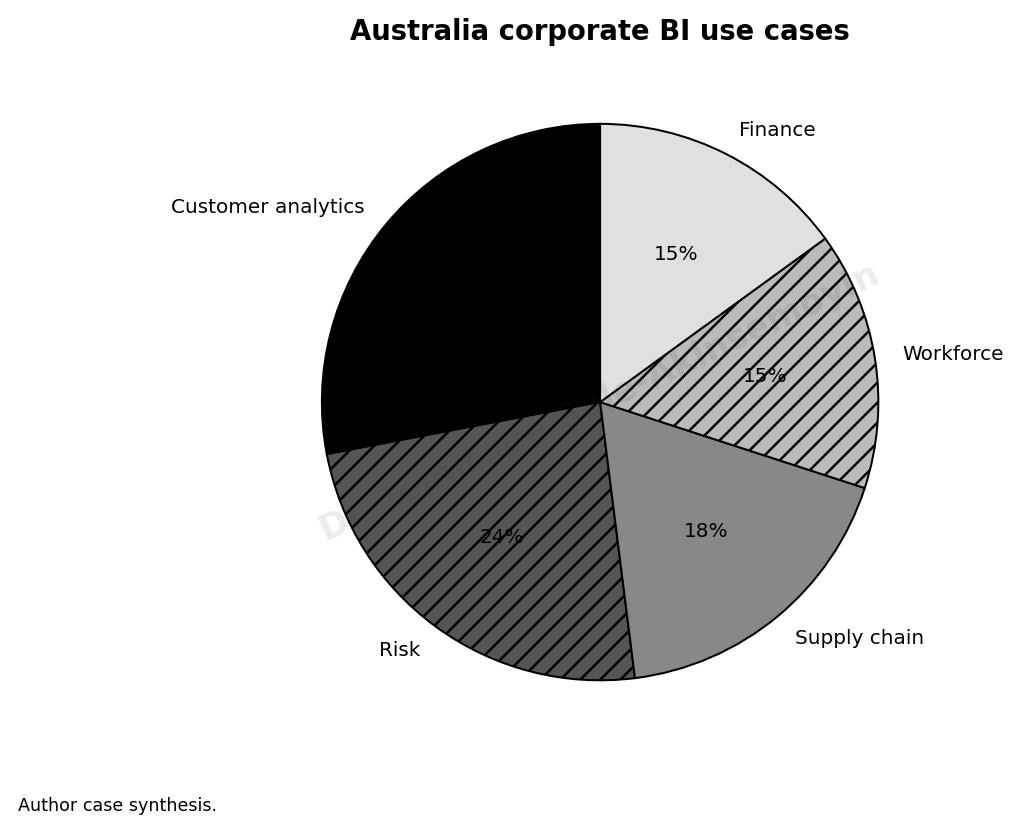

Figure 4. Australia corporate BI use cases.

Source: Author case synthesis.

Table 1. Australia and Georgia corporate BI comparison

| Dimension | Australia emphasis | Georgia emphasis |

| Market setting | Large advanced economy with mature data governance | Emerging digital hub with strong GovTech momentum |

| Corporate priority | AI investment, productivity, and risk controls | Enterprise ICT adoption and digital finance |

| Constraint | Skills, privacy, legacy systems | Scale, data depth, and SME capability |

| Opportunity | Responsible AI and predictive operations | Digital services, fintech, logistics and regional hub strategy |

Note. Table prepared; black-and-white NYCAR publication format.

Chapter 4: Georgia: Digital Transformation, Enterprise ICT, and Market modernization

4.1 Georgia’s digital transition as a corporate case

Georgia’s enterprise digital transition and the uneven pace of institutional capability cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For Georgia’s digital transition, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through Georgia’s digital transition: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

4.2 Georgian evidence on enterprise ICT adoption

The section on georgian evidence on enterprise ict adoption places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for georgian evidence on enterprise ict adoption needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under georgian evidence on enterprise ict adoption, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The reform rhythm should be deliberate. A firm should test a manageable intelligence routine, compare the report with actual managerial behavior, remove data noise, and strengthen the handoff between analysts and decision owners. Only then should it expand the system.

4.3 Management choices in a smaller emerging market

Management choices around Georgia’s enterprise digital transition and the uneven pace of institutional capability begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of Georgia’s digital transition, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for Georgia’s digital transition links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

4.4 Risks in uneven capability and investment timing

The section on risks in uneven capability and investment timing places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for risks in uneven capability and investment timing needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under risks in uneven capability and investment timing, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for risks in uneven capability and investment timing is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

4.5 What Georgian experience teaches about disciplined growth

Institutional learning is the part of Georgia’s enterprise digital transition and the uneven pace of institutional capability that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in Georgia’s digital transition also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for Georgia’s digital transition is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

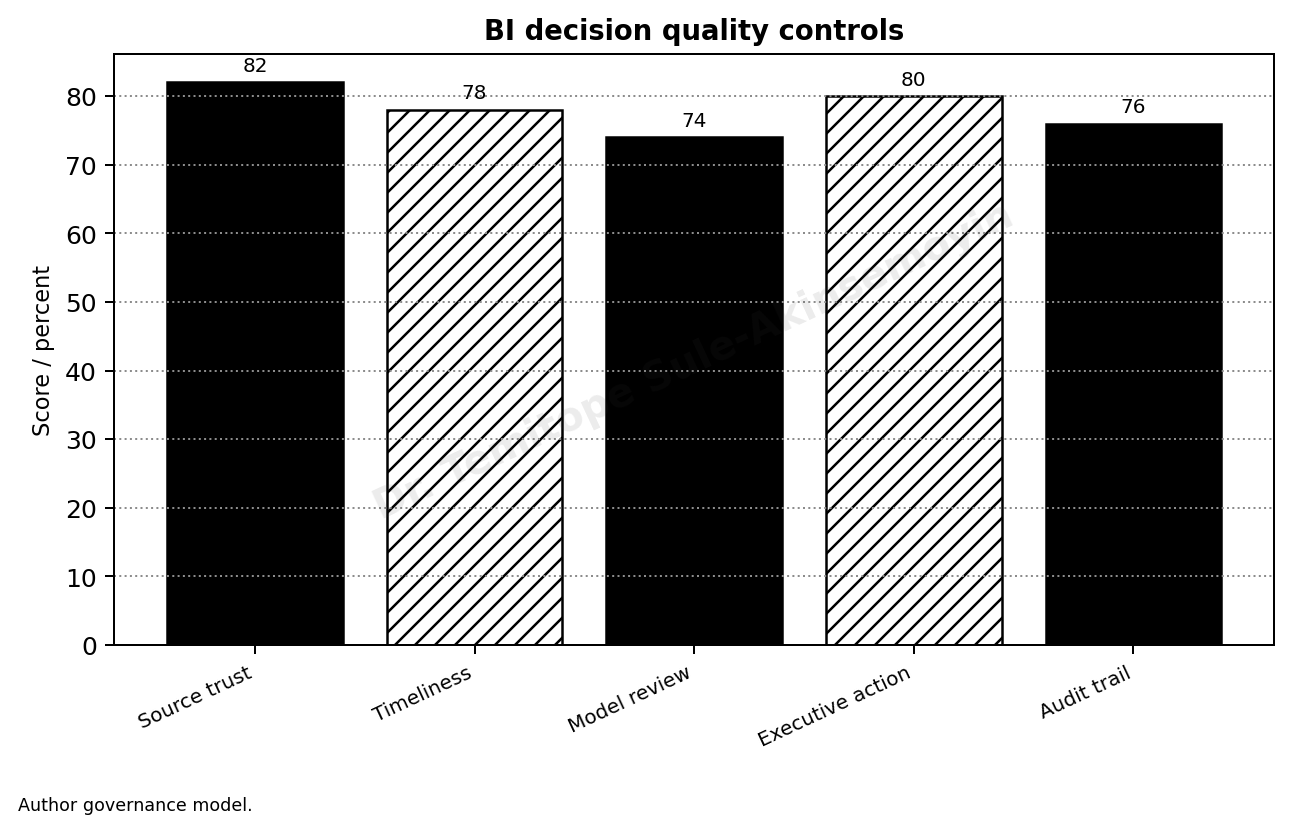

Figure 5. BI decision quality controls.

Source: Author governance model.

Read also: Strategic Branding and Intellectual Property in Business

Chapter 5: Corporate Case Studies in Banking, Retail, Logistics, and Public-Private Systems

5.1 Case evidence beyond the dashboard

Corporate case evidence from banking, retail, logistics, and public-private systems cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For corporate case evidence, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through corporate case evidence: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

5.2 Evidence from banking, retail, logistics, and public systems

The section on evidence from banking, retail, logistics, and public systems places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for evidence from banking, retail, logistics, and public systems needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under evidence from banking, retail, logistics, and public systems, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for evidence from banking, retail, logistics, and public systems is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

5.3 How corporate teams turn signals into decisions

Management choices around corporate case evidence from banking, retail, logistics, and public-private systems begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of corporate case evidence, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for corporate case evidence links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

5.4 Cross-sector risks in data sharing and accountability

The section on cross-sector risks in data sharing and accountability places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for cross-sector risks in data sharing and accountability needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under cross-sector risks in data sharing and accountability, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for cross-sector risks in data sharing and accountability is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

5.5 Learning from cases without copying them mechanically

Institutional learning is the part of corporate case evidence from banking, retail, logistics, and public-private systems that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in corporate case evidence also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for corporate case evidence is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

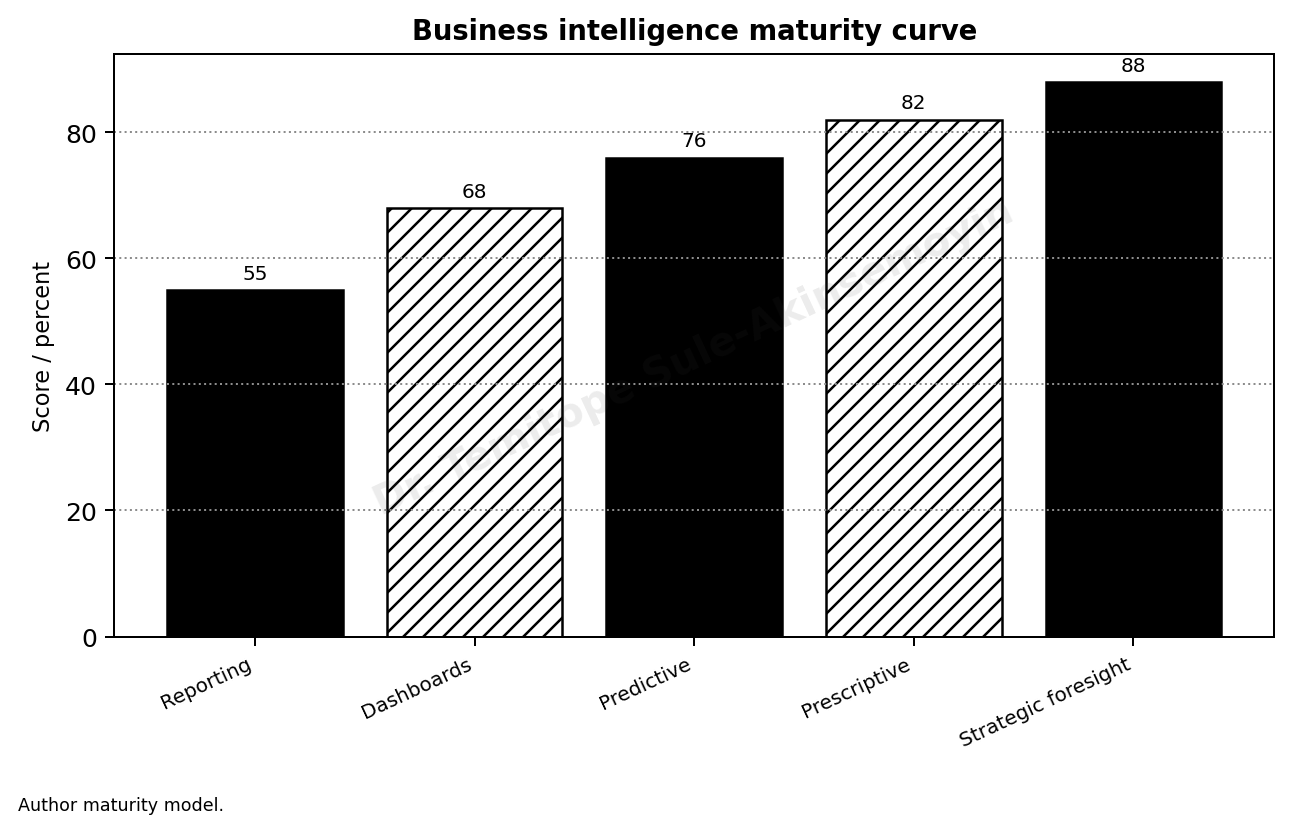

Figure 6. Business intelligence maturity curve.

Source: Author maturity model.

Chapter 6: Data Quality, Dashboards, and the Politics of Measurement

6.1 The hidden cost of poor data quality

The politics of data quality, dashboards, and executive measurement cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For data quality and dashboards, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through data quality and dashboards: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

6.2 Evidence from measurement, dashboards, and operating records

The section on evidence from measurement, dashboards, and operating records places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for evidence from measurement, dashboards, and operating records needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under evidence from measurement, dashboards, and operating records, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for evidence from measurement, dashboards, and operating records is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

6.3 Measurement, incentives, and operational truth

Management choices around the politics of data quality, dashboards, and executive measurement begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of data quality and dashboards, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for data quality and dashboards links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

6.4 Risks of cosmetic reporting and weak ownership

The section on risks of cosmetic reporting and weak ownership places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for risks of cosmetic reporting and weak ownership needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under risks of cosmetic reporting and weak ownership, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The corporate world does not need more polished numbers that no one owns. It needs evidence that reaches the person with authority to act. The intelligence cycle is mature only when a signal moves through interpretation, decision, execution, and review without disappearing into committee language.

6.5 Making evidence useful after the meeting ends

Institutional learning is the part of the politics of data quality, dashboards, and executive measurement that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in data quality and dashboards also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for data quality and dashboards is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

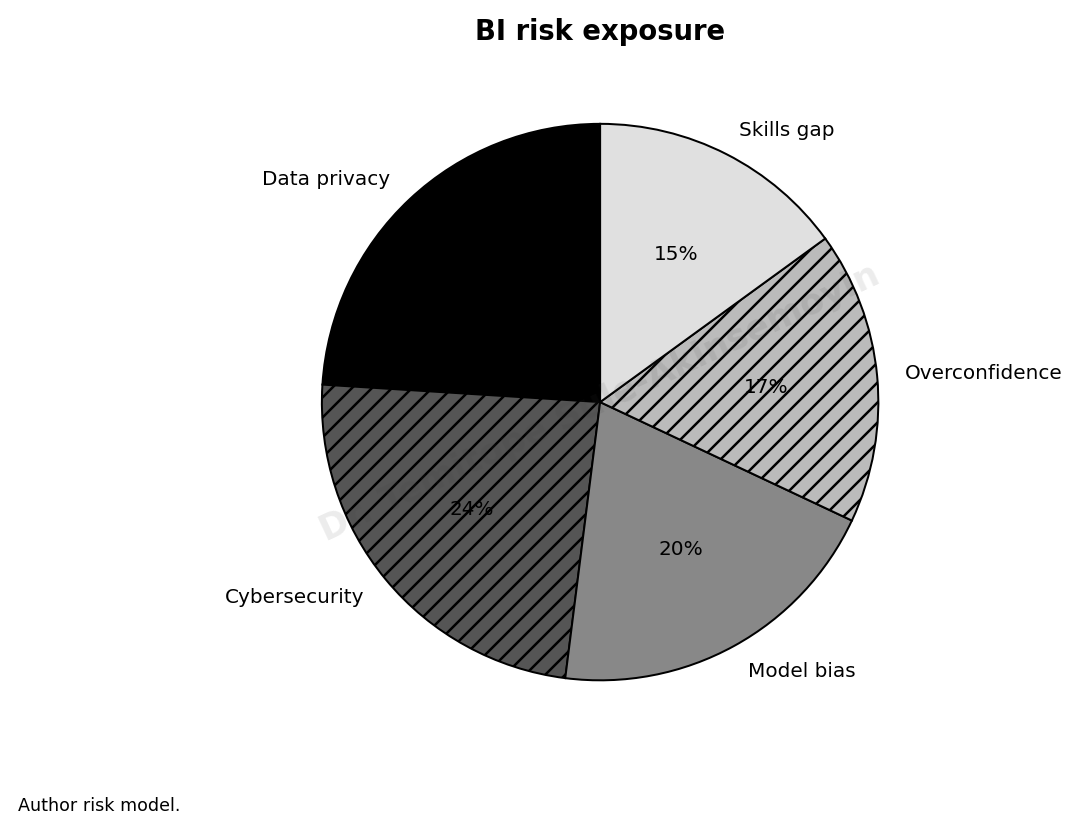

Figure 7. BI risk exposure.

Source: Author risk model.

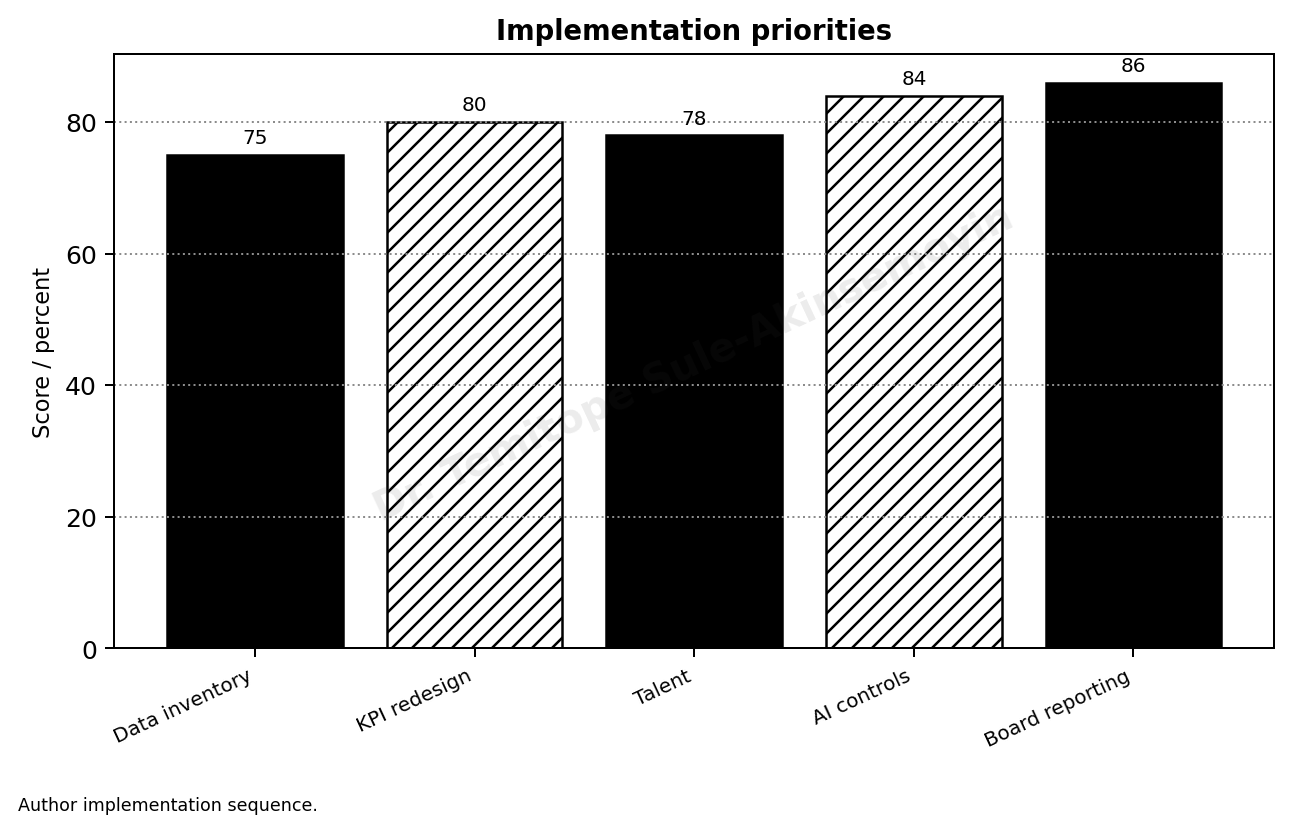

Figure 8. Implementation priorities.

Source: Author implementation sequence.

Table 2. Strategic BI decision protocol

| Step | Management question | Control |

| Define | What decision must change? | Decision charter |

| Collect | Which data are reliable? | Source register |

| Analyze | What model or metric is used? | Model review |

| Act | Who owns the decision? | Executive action log |

| Learn | What changed after action? | Outcome review |

Note. Table prepared; black-and-white NYCAR publication format.

Chapter 7: AI, Predictive Analytics, Cyber Risk, and Ethical Intelligence

7.1 AI as a corporate intelligence responsibility

Ai, predictive analytics, cyber exposure, and ethical business intelligence cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For AI and predictive analytics, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through AI and predictive analytics: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

7.2 Evidence on predictive analytics, cyber risk, and consent

The section on evidence on predictive analytics, cyber risk, and consent places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for evidence on predictive analytics, cyber risk, and consent needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under evidence on predictive analytics, cyber risk, and consent, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for evidence on predictive analytics, cyber risk, and consent is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

7.3 Management controls for automated judgment

Management choices around AI, predictive analytics, cyber exposure, and ethical business intelligence begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of AI and predictive analytics, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for AI and predictive analytics links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

7.4 Ethical risks in data-driven competition

The section on ethical risks in data-driven competition places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for ethical risks in data-driven competition needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under ethical risks in data-driven competition, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for ethical risks in data-driven competition is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

7.5 Review routines for intelligent systems

Institutional learning is the part of AI, predictive analytics, cyber exposure, and ethical business intelligence that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in AI and predictive analytics also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for AI and predictive analytics is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

Chapter 8: Strategic BI Formula and Comparative Readiness Model

8.1 Why the readiness model must remain practical

Comparative readiness scoring and the danger of false precision cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For readiness scoring, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through readiness scoring: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

8.2 Evidence behind the readiness variables

The section on evidence behind the readiness variables places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for evidence behind the readiness variables needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under evidence behind the readiness variables, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for evidence behind the readiness variables is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

8.3 Turning the formula into a decision conversation

Management choices around comparative readiness scoring and the danger of false precision begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of readiness scoring, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for readiness scoring links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

8.4 Risks of over-scoring and false precision

The section on risks of over-scoring and false precision places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for risks of over-scoring and false precision needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under risks of over-scoring and false precision, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for risks of over-scoring and false precision is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

8.5 How the model should guide learning

Institutional learning is the part of comparative readiness scoring and the danger of false precision that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in readiness scoring also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for readiness scoring is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

Chapter 9: Implementation Blueprint for Australia and Georgia-Informed Corporations

9.1 Implementation as ordinary corporate work

Implementation discipline across australian and georgian corporate settings cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For implementation practice, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through implementation practice: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

9.2 Implementation evidence from market comparison

The section on implementation evidence from market comparison places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for implementation evidence from market comparison needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under implementation evidence from market comparison, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for implementation evidence from market comparison is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

9.3 Decision forums, budgets, and data owners

Management choices around implementation discipline across Australian and Georgian corporate settings begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of implementation practice, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for implementation practice links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

9.4 Rollout risks in Australia and Georgia-informed practice

The section on rollout risks in australia and georgia-informed practice places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for rollout risks in australia and georgia-informed practice needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under rollout risks in australia and georgia-informed practice, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for rollout risks in australia and georgia-informed practice is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

9.5 Institutional learning after adoption

Institutional learning is the part of implementation discipline across Australian and Georgian corporate settings that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in implementation practice also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for implementation practice is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

Table 3. BI risk register

| Risk | Corporate symptom | Mitigation |

| Dashboard theatre | Reports rise while decisions do not change | Decision-based KPI review |

| Data silos | Competing truths across departments | Enterprise data governance |

| AI opacity | Unexplainable recommendations | Model documentation and human review |

| Cyber exposure | More data increases attack surface | Security-by-design and access control |

| Cultural resistance | Managers defend intuition against evidence | Executive training and incentives |

Note. Table prepared; black-and-white NYCAR publication format.

Chapter 10: Final Position: Intelligence That Changes Decisions

10.1 What strategic BI should finally mean

The final meaning of intelligence that changes corporate decisions cannot be solved by buying more technology or adding another dashboard to the executive meeting. The real issue is whether the organization has enough discipline to convert signals into decisions that can survive scrutiny.

For final corporate judgment, the Australia-Georgia comparison is useful because the two markets test different forms of corporate discipline. Australia shows how mature systems can still struggle with overconfidence, model risk, and executive interpretation; Georgia shows how fast digital adoption must be matched with skills, governance, and institutional memory.

This chapter reads business intelligence through final corporate judgment: what leaders know, what they do with that knowledge, who is permitted to challenge it, and whether the decision changes before cost, risk, or lost opportunity forces a correction.

10.2 Evidence and judgment in the final corporate position

The section on evidence and judgment in the final corporate position places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for evidence and judgment in the final corporate position needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (World Bank, 2022). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under evidence and judgment in the final corporate position, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for evidence and judgment in the final corporate position is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

10.3 Decisions that prove intelligence is real

Management choices around the final meaning of intelligence that changes corporate decisions begin with decision rights. Someone must own the data source, someone must own interpretation, and someone must own the action that follows from the intelligence.

In matters of final corporate judgment, divided responsibility should not become an excuse for inaction. Data teams may prepare the evidence, but executives must decide how the evidence affects risk, capital, customers, operations, and accountability.

A stronger routine for final corporate judgment links every intelligence product to a decision owner, a review date, a risk note, and a record of what changed. That discipline separates serious BI from attractive reporting.

10.4 Limits of data when judgment is weak

The section on limits of data when judgment is weak places business intelligence inside executive work rather than software display. Australia and Georgia offer a useful contrast because corporate leaders in both settings need evidence, but they do not face the same regulatory maturity, digital depth, capital structure, or managerial habits. The question is whether intelligence changes the quality of a decision before the market, regulator, lender, customer, or board exposes the weakness.

The evidence for limits of data when judgment is weak needs careful interpretation. Public data can show digital adoption, investment climate, and regulatory direction, but it cannot automatically prove stronger corporate judgment (Australian Government, 2023). That is why the analysis reads evidence beside decision rights, data quality, staff capability, and executive accountability. Intelligence is useful only when it narrows uncertainty without pretending that uncertainty has disappeared.

Under limits of data when judgment is weak, accountability should be written into the meeting routine. The evidence owner should state the limit of the data, the decision owner should state the action to be taken, and the review owner should return later with proof of what changed. That habit turns intelligence from presentation into governance.

The safeguard for limits of data when judgment is weak is controlled use. The firm should verify the source, test the assumption, document the model limit, protect sensitive data, and revisit the result after the decision is made. That discipline prevents mature Australian organizations from confusing technical capacity with wisdom, and it prevents Georgian firms from scaling digital tools faster than internal governance can carry them.

10.5 Final position for corporate leaders

Institutional learning is the part of the final meaning of intelligence that changes corporate decisions that determines whether BI becomes part of corporate habit. A company learns only when prior intelligence changes the next budget, meeting, product decision, staffing plan, risk control, or market choice.

Learning in final corporate judgment also requires humility. A model, dashboard, or country comparison may work for one sector or quarter and fail when regulation, staff capacity, customer behavior, or market conditions shift.

The practical lesson for final corporate judgment is that intelligence earns its place through better timing and clearer responsibility. It should help leaders act earlier, explain better, correct faster, and avoid treating data as a substitute for judgment.

References

Australian Bureau of Statistics. (2024). Business characteristics surveys consultation. https://consult.abs.gov.au/industry-statistics/business-characteristics-surveys-consultation/

Australian Government. (2023). Data and Digital Government Strategy: 2023-2030. https://www.dataanddigital.gov.au/

Davenport, T. H., & Harris, J. G. (2017). Competing on analytics: The new science of winning. Harvard Business Review Press.

International Finance Corporation & World Bank. (2023). Georgia Country Private Sector Diagnostic. https://www.ifc.org/

Marr, B. (2022). Data strategy: How to profit from a world of big data, analytics and artificial intelligence. Kogan Page.

National Statistics Office of Georgia. (2025). Use of information-communication technologies in enterprises – 2024. https://www.geostat.ge/

Reserve Bank of Australia. (2025). Technology investment and AI: What are firms telling us? https://www.rba.gov.au/publications/bulletin/2025/nov/technology-investment-and-ai-what-are-firms-telling-us.html

World Bank. (2022). Georgia: Promoting digital transformation through GovTech. https://thedocs.worldbank.org/

World Bank. (2026). Digital and AI. https://www.worldbank.org/ext/en/topic/digital-and-ai