The analysis is intentionally managerial, asking what disciplined leaders can do when both expectations and constraints are high. The paper is written for professional readers who need strategic guidance that is both intellectually serious and operationally usable.

Research Publication by Theodora Kelechi Anurukem

New York Center for Advanced Research (NYCAR)

Publication No.: NYCAR-TTR-2026-RP005

Date: June 2026

DOI: https://doi.org/10.5281/zenodo.20356825

Peer Review Status: This research paper was reviewed and approved under the internal editorial peer review framework of the New York Center for Advanced Research (NYCAR) and The Thinkers’ Review. The process was handled independently by designated Editorial Board members in accordance with NYCAR’s Research Ethics Policy.

Copyright © June 2026 New York Center for Advanced Research (NYCAR) and Theodora Kelechi Anurukem. All rights reserved.

Abstract

Sustainability reaches many small firms as a demand from outside the business. A buyer wants waste records. A lender asks about risk. A customer wants proof that labor and sourcing claims are not just words. Inside the firm, records are poor, one manager handles sales and compliance, and the budget is already under strain. That is the condition the analysis takes seriously. Rather than treating constraint as an excuse to avoid responsibility, it reads constraint as the very setting in which responsible strategy has to be designed.

At the center of the argument is a simple claim: a resource-constrained firm needs a disciplined starting point before it needs an ESG system. Work begins by choosing a material issue that touches cost, risk, customers, workers, or regulation. It then has to be narrowed into an action the firm can afford, assigned to someone who keeps evidence, reviewed through a routine the firm already uses, and communicated without exaggeration. A claim that cannot be proved should not be made.

Practically, the model is meant to discipline managerial judgment rather than decorate the firm’s public language. It links material focus, staged ambition, control routines, capability extension, and evidence-based communication. Its purpose is not to make a small firm look like a large one, but to help managers, buyers, lenders, and advisers judge whether a constrained firm is making credible progress on work that matters and can be sustained.

Keywords: sustainable strategy, resource-constrained firms, SMEs, materiality, ESG evidence, management control, sustainability communication

Table of Contents

List of Tables

Table 1. Resource-constraint pressure points and strategic response 11

Table 2. Literature logic for the sustainable strategy model 16

Table 3. Diagnostic scoring guide for the sustainable strategy model 27

Table 4. Implementation roadmap for resource-constrained firms 42

List of Figures

Figure 1. Five-discipline model for sustainable strategy under constraint 26

Figure 2. Implementation cycle from issue selection to staged expansion 30

Figure 3. Governance map linking the constrained firm with external actors 41

Chapter 1: Introduction

1.1 Background to the Study

Sustainability pressure now reaches firms that were never built for formal sustainability reporting. A regional supplier receives a buyer questionnaire. A small manufacturer receives a request for waste data. A service firm is asked about labor practice, sourcing, and risk. Inside the business, the request lands on the desk of an owner-manager, operations head, or accounts officer who already handles production delays, customers, payroll, and supplier disputes. The language of sustainability sounds orderly from outside the firm, yet inside it lands as one more demand for evidence in a business already operating close to its limits.

Resource-constrained firms do not reject sustainability because responsibility is unfamiliar. Many owners understand waste, safety, energy cost, worker retention, customer trust, and supplier risk through daily experience. The problem is translation. Informal knowledge does not satisfy a buyer audit. A supervisor’s memory does not satisfy a lender. A promise does not satisfy a responsible customer. The firm has to convert practical knowledge into evidence without creating a system it lacks the staff and money to maintain.

Large-firm sustainability practice often assumes a reporting unit, consultant support, digital platforms, board attention, and spare administrative capacity. Smaller firms operate differently. Evidence sits in invoices, repair notes, training sheets, WhatsApp messages, supplier files, and the memory of workers who know the process. That evidence is usable, but only after it is gathered, assigned, reviewed, and tied to decisions. Responsible strategy in this setting begins with ordinary records rather than public language.

Strategy scholarship helps explain why this starting point matters. Barney’s resource-based view reminds researchers that firms act through resources and capabilities they can organize (Barney, 1991). Hart’s natural-resource-based view connects environmental responsibility with capabilities and competitive advantage (Hart, 1995). Those arguments are useful, but a constrained firm needs translation. Capability here is not an ESG department but the practical ability to identify a material issue, keep a record, review it, and act before speaking publicly.

Such translation is the central concern of the analysis. Sustainability is treated neither as image nor as burden. Instead, it is treated as managerial discipline exercised under constraint. A firm that cannot afford a formal ESG system still has to know what matters, where evidence sits, who owns the work, and which claims are safe. This position gives smaller firms a serious role without excusing weak practice.

1.2 Problem Statement

At issue is the gap between sustainability pressure and managerial capacity in resource-constrained firms. External actors increasingly ask for evidence of environmental and social responsibility. Buyers ask about waste, emissions, labor, traceability, and sourcing. Lenders ask whether risk is being controlled. Customers and communities judge whether claims match conduct. Yet many firms receiving those requests lack clean records, formal procedures, specialist staff, or finance for system building.

That gap produces two forms of risk, because overstatement damages trust when claims outrun evidence, while silence creates the impression that the firm has no responsibility position at all. A supplier that copies broad sustainability language without records exposes itself during buyer review. A firm that refuses to speak because its records are weak loses the chance to show serious early-stage work. Neither response serves the firm or its stakeholders.

More precisely, the difficulty is not lack of interest. The difficulty is weak sequence. A constrained firm needs to identify a material issue before it writes a policy. It needs an owner before it promises progress. It needs a record before it releases a claim. It needs staged ambition before it announces a target. Without this sequence, sustainability becomes an administrative performance rather than managerial practice.

NYCAR research standards require the paper to engage that tension directly. A graduate research paper cannot rely on broad declarations about sustainability. It has to show how responsibility operates inside a firm with cash pressure, thin staff, weak data trails, and external demands. It also has to respect the firm’s agency. Constraint is real; so is managerial choice.

1.3 Aim, Objectives, and Research Questions

The paper develops a practical model for sustainable strategy in resource-constrained firms. It focuses on firms that face sustainability demands but lack the administrative depth of larger organizations. Its purpose is to show how credible action begins when capacity is thin and evidence remains incomplete.

Its objectives are to assess sustainability pressure facing constrained firms; explain why generic ESG systems often fit poorly; connect sustainability strategy to materiality, sequence, records, capability, and communication; and present a model that managers and external actors can use without pretending that small firms possess large-company resources. The model is designed for managerial use, not symbolic display.

Several practical questions guide the work. How should a constrained firm select a sustainability issue? What kind of ambition fits limited resources? Which records turn informal practice into evidence? How should a firm communicate progress without exaggeration? How should buyers, lenders, and advisers assess constrained firms fairly while still requiring proof?

Such questions keep the paper close to management. The concern is not whether sustainability is desirable. The concern is how a firm with limited cash, labor, time, and data can practice responsibility in a way that survives audit, buyer scrutiny, and daily operating pressure.

1.4 Significance of the Study

For managers, the study matters because sustainability pressure often arrives before the firm has an internal method. A manager knows which process creates waste, which supplier creates risk, which machine consumes energy, or which work practice creates safety exposure. Knowledge of the issue is not enough. The firm needs a disciplined way to select, record, review, and communicate. The analysis gives that discipline a practical form.

For larger buyers, the argument also matters. Supply-chain sustainability often transfers demands downward. A buyer asks for evidence from a supplier without providing time, templates, training, or finance. That practice produces paperwork more easily than progress. A better standard asks for material issue selection, staged action, and evidence that fits the supplier’s capacity. This is more rigorous than accepting copied policy language.

Lenders and advisers gain from the same logic. A lender assessing risk needs evidence, not aspiration. An adviser supporting an SME needs to build records, not decorate the firm with language. The paper offers a method for judging credibility through action and evidence. It also shows where support, finance, or training unlocks better practice.

Academically, the study joins strategy and sustainability debates through the question of constraint. ESG research often asks whether sustainability improves performance. Strategy research asks how firms organize resources. SME research asks how smaller firms survive pressure. The analysis brings those concerns together and asks how responsibility becomes credible when the firm is stretched.

1.5 Scope and Delimitations

The scope centers on small and medium-sized firms, local suppliers, and businesses operating under finance, staffing, data, and infrastructure limits. The argument applies across sectors, but the examples draw mainly from manufacturing, supply, trading, and service firms because those settings expose the record problem clearly. Energy use, waste, labor practice, supplier evidence, and buyer pressure appear repeatedly in such firms.

Conceptually, the paper remains applied. It does not report field interviews, survey data, or proprietary firm records. It draws on strategy, sustainability, ESG, management control, and SME literature to build a practical model. Illustrative scenarios are used as analytical examples. They do not represent hidden field data.

The argument does not hold that constrained firms deserve lower ethical expectations. It holds that responsibility has to be made operational. A firm cannot be serious about sustainability if it speaks beyond its evidence. It also cannot be dismissed because it lacks a corporate reporting unit. Credible progress under constraint is the standard.

Table 1. Resource-constraint pressure points and strategic response

| Pressure point | Inside the firm | Strategic response |

| Buyer evidence demand | Customer asks for waste, sourcing, safety, or energy records before a reporting system exists. | Start with one material record tied to the highest-risk buyer concern. |

| Thin staffing | One manager handles sales, compliance, suppliers, and documentation. | Assign a narrow owner role linked to existing work. |

| Weak data trail | Invoices, logs, and supervisor notes exist but remain unorganized. | Turn existing documents into a simple evidence file reviewed on schedule. |

| Cash pressure | Needed improvement is known but delayed by operating cost and payment cycles. | Stage ambition by cost, risk, and available finance. |

| Communication risk | The firm wants to look responsible before proof is ready. | Speak only about completed action, evidence, limits, and next steps. |

Chapter 2: Literature Review

2.1 Sustainable Strategy and Resource Constraint

Sustainable strategy is often described as the integration of economic, social, and environmental responsibility into firm direction. Elkington’s triple-bottom-line idea widened managerial attention beyond profit alone (Elkington, 1998). Hart’s natural-resource-based view connected environmental conduct to capability and strategic advantage (Hart, 1995). Those concepts remain useful, but resource-constrained firms require a more practical reading. They do not start from the question of how to report sustainability. They start from the question of how to act credibly while operating with limited capacity.

Resource constraint alters the meaning of strategy. A firm with thin staff and limited cash does not need a longer list of commitments. It needs sharper selection. It has to decide which issue matters now, which action is manageable, which record exists, and which claim is safe. Such decisions are strategic because they protect buyer access, cost control, worker trust, compliance, and reputation.

The resource-based view offers a strong anchor here. Firms differ because they possess different resources and organize them differently (Barney, 1991). In a constrained firm, sustainability capability rarely appears as a formal office. It appears as an ability to use existing routines: maintenance checks, procurement files, training sheets, incident reports, energy bills, waste tickets, customer complaints, and supplier invoices. Strategic value emerges when those ordinary records are organized for review and decision.

This reading also protects the paper from romanticizing constraint. Scarcity does not automatically create discipline. Many firms under pressure drift into weak claims or fragmented records. The model developed here treats constraint as a reason for sharper management, not as a badge of virtue.

2.2 ESG Performance and Firm Outcomes

Across the ESG literature, evidence shows that responsible practice links with performance under certain conditions. Orlitzky, Schmidt, and Rynes (2003) connected corporate social performance and financial performance. Friede, Busch, and Bassen (2015) reviewed a large body of ESG studies and reported broad support for positive associations. Handoyo (2024) adds institutional context by showing that regulatory quality and government effectiveness shape ESG-performance relationships in ASEAN settings.

The lesson for constrained firms is cautious. ESG language does not create performance. Practice, governance, process, and evidence matter. A small firm that reduces waste, improves safety records, strengthens supplier files, or protects buyer trust creates value through operations. The value does not arise from the acronym; it arises from better control of a material issue. Eccles, Ioannou, and Serafeim (2014) reach a similar conclusion at larger scale, finding that firms which embed sustainability into their processes develop different routines and performance paths over time, which supports the present focus on practice rather than language.

Performance should therefore be read in concrete terms. A waste routine protects margin. A labor record protects continuity and trust. A supplier file protects buyer access. An energy review supports cost management. A careful statement protects reputation by refusing unsupported claims. These are not dramatic outcomes, but they matter to firms working with thin buffers.

Context also matters. A firm in a setting with unreliable electricity, limited finance, and weak public support faces different implementation costs than a firm with better infrastructure. ESG pressure without context becomes unfair. Evidence-based staging gives the firm a way to respond without false equivalence. Ukko, Nasiri, Saunila, and Rantala (2019) add that sustainability strategy can shape how other strategic choices convert into financial performance, a reminder that the value of responsible practice is conditional rather than automatic.

2.3 Materiality and Strategic Selection

Materiality is the discipline that prevents scattered sustainability work. A constrained firm cannot act on every issue at once. It needs to identify the issue tied most directly to cost, risk, customers, workers, regulation, or trust. In a food processor, materiality points toward waste, energy, safety, packaging, or traceability. In a logistics firm, fuel, driver welfare, maintenance, and route discipline become more relevant. In a service firm, labor practice, data handling, procurement, and customer trust carry weight.

Materiality also protects credibility. A firm that speaks broadly while ignoring its highest-risk issue invites doubt. A firm that selects one material issue and builds evidence earns a stronger position. The size of the promise matters less than the strength of the record. Strategic selection is therefore both managerial and ethical.

Starting small does not mean thinking small. It means refusing the illusion that broad language solves operational exposure. A firm that learns to manage one material issue well gains a repeatable method. Once it knows how to name the issue, assign the owner, keep the record, and communicate carefully, it can extend the same discipline to another issue. Schaltegger and Wagner (2011) note that sustainability and entrepreneurship interact, which means a well-chosen material issue can open new value rather than only contain risk.

The analysis treats materiality as the entry point into the model. Without material focus, staged ambition becomes arbitrary. Control routines track the wrong thing. Capability extension lacks direction. Communication becomes cosmetic. Materiality tells the firm where serious work begins.

2.4 Management Control and Evidence Discipline

Management control is often less attractive than sustainability vision, yet it is the place where credibility is built. Hasu (2025) links sustainability strategy, SME performance, and management control systems. For constrained firms, the implication is direct: responsibility needs records, ownership, review, and action. A policy without a record is weak. A record without review is storage. Review without action is ceremony.

Evidence discipline begins with ordinary documents. An energy bill, maintenance sheet, supplier invoice, incident note, training attendance sheet, or waste ticket can become sustainability evidence when organized. The firm does not need to buy a complex platform before it begins. It needs a basic file, a named owner, a review date, and a decision rule.

Control also teaches restraint. A manager who sees the record knows which claim is ready and which claim is premature. A firm with only one month of waste records should not announce a broad reduction target. It can state that data collection has begun, explain the material issue, and report the next review date. That kind of limited statement is more credible than a large claim without proof.

Inside constrained firms, control has to fit the existing rhythm of work. A monthly operations meeting, supplier review, finance review, or maintenance meeting can carry the sustainability question. The point is not to create another administrative burden. The point is to insert responsibility into decisions already being made.

2.5 Legitimacy, Communication, and Greenwashing Risk

Legitimacy is earned through alignment between claim and practice. Workers notice whether safety claims match conditions. Buyers notice whether supplier evidence is available. Lenders notice whether risk is named and controlled. Communities notice whether environmental effects are ignored. A constrained firm does not escape judgment because it is small.

Communication risk grows when firms use language faster than practice. A buyer wants confidence; the firm writes a broad statement. A lender wants risk assurance; the firm overstates control. An adviser wants the document to sound professional; the wording becomes larger than the evidence. This is how greenwashing enters smaller firms. It does not always begin with deception. It begins with pressure, imitation, and weak records.

Bansal and DesJardine (2014) connect sustainability with time. That point is valuable here. Credibility depends not only on what a firm says today but on whether the practice survives review, cost pressure, and staff turnover. A one-time statement without continuity does not create sustainable strategy.

Evidence-based communication gives the firm a safer voice. The firm can say what issue it selected, what action started, what record exists, and what remains under review. It can state limits without surrendering responsibility. Such restraint reads as expert management rather than weakness.

2.6 Literature Synthesis

Across the literature, the concepts are strong, but the constrained firm still needs a working sequence. Resource-based strategy explains why capability matters. ESG research shows that sustainability-performance links depend on practice and context. Materiality literature explains why selection matters. Management-control work explains why records and review matter. Legitimacy research explains why communication must stay within evidence.

The missing connection is practical sequence. A stretched firm cannot begin everywhere. It needs a material issue, staged ambition, a control routine, a capability base, and careful communication. This sequence does not dilute responsibility. It makes responsibility usable.

Several tensions remain. Buyers demand evidence but often transfer cost downward. Lenders want risk reduction but often hesitate to finance the improvements that reduce risk. Advisers write language more easily than they build records. Managers know operational problems but lack a method for turning knowledge into evidence. The model developed in the analysis responds to those tensions.

The literature therefore supports a disciplined position: sustainable strategy in constrained firms begins with a material issue and becomes credible only when evidence, ownership, review, and restraint are present.

Table 2. Literature logic for the sustainable strategy model

| Literature stream | Lesson for constrained firms | Use in the analysis |

| Resource-based strategy | Firms act through resources and capabilities they can organize. | Treats sustainability capacity as an operational question. |

| ESG and performance research | Responsible practice has value when linked to process and governance. | Connects sustainability to cost, risk, buyer access, finance, and trust. |

| Management control research | Evidence depends on records, review, ownership, and action. | Builds the control-routine discipline. |

| Legitimacy and communication research | Claims create trust only when supported by evidence over time. | Supports restraint in sustainability communication. |

2.7 Buyer Power and Supply-Chain Pressure

Supply-chain pressure is one of the strongest routes through which sustainability reaches constrained firms. A large buyer sets a requirement, and a smaller supplier has to respond even when systems are thin. The demand can involve waste handling, worker safety, emissions data, supplier codes, packaging standards, or sourcing evidence. The buyer often treats the request as routine compliance. For the supplier, the same request becomes a managerial event because it requires documents, time, and internal coordination.

Power matters here because the supplier rarely negotiates from an equal position. Loss of the buyer threatens revenue, cash flow, and worker stability. This dependence encourages quick agreement even when the firm lacks records. A supplier says yes, then searches through invoices, messages, and supervisor notes to assemble proof. The risk is not laziness. The risk is that pressure produces a document faster than it produces management discipline.

Expert-level sustainability assessment has to read this power relation. A buyer that demands evidence has a legitimate interest in responsible supply. Yet demand without support creates brittle compliance. Better supplier assessment asks what issue is material, which record exists, who owns it, what action followed, and what support improves the next stage. This kind of questioning is stricter than accepting broad statements because it forces the supplier to show how responsibility enters the operation.

The paper’s model therefore treats buyer pressure as both an opportunity and a risk. Pressure can make hidden operational exposure visible. It can also push firms into overclaiming. The difference depends on whether the demand is translated into evidence, ownership, and review. A buyer that asks for those elements helps the supplier become more reliable. A buyer that asks only for forms creates paper compliance.

2.8 Finance, Cash Flow, and the Cost of Evidence

Sustainability practice has a cost structure. Metering energy, replacing equipment, improving waste handling, documenting training, screening suppliers, and organizing records all require time and money. Large firms absorb those costs through administrative capacity. Smaller firms experience them as trade-offs against payroll, inventory, repairs, and customer delivery. A sustainability demand that ignores cash flow misreads the firm.

Finance shapes ambition. A firm can begin with records and routine changes, but capital-intensive improvements require funding. A manufacturer can track energy use before it replaces machinery. A food processor can record waste before it purchases improved packaging equipment. A supplier can build a sourcing file before it pays for full audit support. Staged ambition is not a retreat from responsibility. It is a financing reality translated into management sequence.

Lenders therefore belong in the discussion. If a lender claims to value lower environmental and social risk, the assessment should recognize the finance needed to reduce that risk. A small loan for metering, training, safer storage, or record systems can change the firm’s ability to produce evidence. Without finance, the firm remains trapped between expectation and capacity.

Cash flow also affects record quality. A firm under payment stress prioritizes urgent operations. Documentation suffers because immediate survival takes attention. This does not justify weak records, but it explains why a simple evidence system has greater value than a heavy reporting demand. The model favors records that fit ordinary management because that is where constrained firms have a realistic chance of sustaining practice.

2.9 Staff Capacity and Organizational Learning

Staff capacity is not only a headcount problem. It is also a knowledge and role problem. A constrained firm can employ capable people and still fail to convert knowledge into evidence. The production supervisor knows where scrap appears. The accounts officer sees energy cost. The procurement worker knows which supplier causes difficulty. The owner-manager hears the buyer’s concern. Unless these fragments are connected, the firm has knowledge without organized sustainability capacity.

Organizational learning begins when those fragments are turned into a routine. A supervisor records the issue. Accounts attach the cost. Procurement checks the supplier file. Management reviews the record. A decision follows. This is the movement from informal knowledge to managerial learning. It does not require a large team. It requires ownership and review.

Training also needs a practical form. A workshop that teaches general sustainability language does little if staff return to the same undocumented process. Training should connect directly to the record. Workers should know what is being tracked, why the issue matters, who receives the record, and what action follows. This approach links skill development to evidence rather than awareness alone.

Staff continuity strengthens the model. In many smaller firms, one knowledgeable employee carries a large share of process memory. That is risky. If the employee leaves, evidence leaves with the person. A simple record system protects institutional memory. It also protects the employee from bearing an invisible workload that management does not recognize.

2.10 Institutional Quality and Context

Institutional quality shapes the cost of sustainable strategy. A firm operating in a setting with reliable electricity, accessible finance, strong enforcement, and stable public records has a different starting position from a firm working with power interruption, weak infrastructure, costly credit, and uneven regulatory follow-through. Handoyo’s (2024) finding on regulatory quality and government effectiveness is therefore useful for constrained-firm analysis. Context affects whether ESG practice produces value and whether firms can gather evidence at reasonable cost.

Poor institutional conditions do not remove responsibility, but they change the work. A firm that experiences unreliable power has to read energy evidence differently from a firm with stable metering. A supplier working without affordable audit support has to build simpler evidence files before formal assurance. A business facing delayed payments has to stage ambition around cash availability. Context is not an excuse; it is the operating ground on which strategy is built.

External actors often ignore this ground. A buyer headquartered in a well-resourced environment requests the same documentation from suppliers operating under weaker conditions. The demand appears neutral. In practice, it transfers administrative cost and reputational risk to the supplier. The analysis’s model answers that problem by asking for evidence tied to material issues and current capacity, while still requiring proof of action.

2.11 Reporting, Evidence, and the Problem of Display

Reporting and evidence are not the same. Reporting is the presentation of information. Evidence is the record that supports it. A resource-constrained firm gets into trouble when reporting outruns evidence. The document looks complete, but the underlying routine is thin. Expert assessment should therefore read behind the report.

Surface presentation can easily outrun substance when a firm is under pressure. A supplier can produce a polished statement before it can trace supplier records, training logs, or waste files. That imbalance is exactly what the research rejects. Credible sustainability practice begins with verifiable action, not with language designed to look complete before the underlying routine exists.

Evidence discipline reverses the order. A record comes before a claim. Review comes before communication. Ownership comes before public commitment. This order is demanding because it slows the impulse to perform responsibility. It also produces a stronger managerial position. A firm that speaks after evidence speaks with authority.

The paper therefore treats reporting as an output, not the center. The center is the evidence routine. Once the routine exists, reporting becomes simpler, safer, and more honest.

Chapter 3: Methodology

3.1 Research Design

Methodologically, the paper uses a qualitative evidence-integrative design. It draws from strategy, sustainability, ESG, management control, and SME scholarship to build a practical model for resource-constrained firms. The design fits the research problem because the paper is not testing a dataset. It is organizing evidence into a usable management method.

The method remains applied rather than abstract. It asks what a constrained firm needs in order to respond credibly to sustainability pressure. That question requires attention to finance, records, staff capacity, buyer pressure, communication, and trust. It also requires refusal of inflated claims. The paper states what it can support and what it cannot prove.

No field survey, interview set, or proprietary company record is claimed. The paper develops a conceptual-applied model for later empirical testing. Its present value lies in disciplined synthesis and managerial usability.

3.2 Source Strategy and Analytical Coding

The source strategy follows the paper’s applied purpose. Each body of literature is read for a managerial question. Resource-based strategy answers what the firm can organize. ESG research answers when responsible practice links to value. Management-control literature answers how evidence becomes usable. Legitimacy research answers why claims require proof. SME scholarship answers how constraint shapes implementation.

Analytical coding is organized around repeated tensions. Capacity appears against expectation. Evidence appears against language. Buyer pressure appears against supplier support. Ambition appears against finance. Communication appears against proof. These tensions become the basis for the five disciplines used later in the model.

The coding logic is simple but demanding. A concept is retained when it helps a manager act, helps a buyer assess, helps a lender read risk, or helps an adviser build records. Concepts that remain too broad for constrained-firm use are translated into operating questions. For example, capability becomes: who owns the record? Materiality becomes: which issue threatens cost, trust, regulation, or buyer access? Legitimacy becomes: what claim can the firm prove?

This method keeps the paper from drifting into abstract sustainability language. Every concept has to return to the firm. That return to practice is the main control on the analysis.

3.3 Evidence Base and Analytical Procedure

The evidence base draws from peer-reviewed literature on resource-based strategy, sustainability, ESG performance, sustainability innovation, management control, legitimacy, and SME practice. Sources are used because they speak to capacity, evidence, performance, routine, communication, or constrained implementation. Work written for large firms is not discarded; it is translated cautiously for smaller firms.

Selection follows a practical logic. A source is useful when it helps answer what a manager should do, what a buyer should ask, what a lender should value, or what a firm should avoid saying. That standard keeps the method close to the paper’s applied purpose.

Analytically, the work identifies repeated tensions across the literature: ambition against capacity, pressure against support, reporting against evidence, communication against proof, and responsibility against overclaiming. Those tensions are organized into five disciplines: material focus, staged ambition, control routines, capability extension, and evidence-based communication.

Each discipline is defined as a test. Material focus asks whether the issue matters to the firm’s exposure. Staged ambition asks whether action fits resources and sequence. Control routines ask whether evidence is recorded and reviewed. Capability extension asks whether existing skills and files are used. Evidence-based communication asks whether claims match records. The procedure stays simple because a model for constrained firms cannot depend on administrative weight the firm cannot carry.

3.4 Reliability of Evidence in Constrained Firms

Evidence in constrained firms is often imperfect. That does not make it useless. The paper treats evidence as a record that can be inspected, repeated, and linked to a decision. A waste ticket, energy bill, incident log, training sheet, or supplier invoice has value when the firm knows where it sits, who keeps it, and how it is reviewed.

Reliability increases through routine. One record taken once has limited value. A record kept every month begins to show pattern. A review note shows that management looked at the record. A corrective action shows that the record influenced practice. This progression matters more than document polish.

External actors should also read evidence with care. A small supplier’s record will not always look like a corporate dashboard. That does not mean the record is weak. Weakness appears when nobody owns it, when dates are missing, when no review takes place, or when communication claims more than the record supports. A plain record with ownership and review can carry more credibility than a polished report without operational connection.

The model’s evidence standard is therefore practical: the record must exist, be owned, be reviewed, and support the claim. Anything less remains vulnerable.

3.5 Methodological Limitations and Field Testing Plan

The method has boundaries. It organizes scholarship into a practical model, but it does not measure firm outcomes. It does not certify environmental performance. It does not prove that every constrained firm will improve through the model. The model remains a disciplined decision tool awaiting field testing.

Field testing should assess whether the five disciplines appear in real firms and which discipline breaks down most often. Interviews with managers can show how buyer demands arrive. Document review can show whether evidence files exist. Buyer interviews can reveal which claims are accepted or rejected. Lender interviews can show whether sustainability records influence risk judgment.

Sector comparison would strengthen the next stage. Manufacturing firms probably show waste and energy as early material issues. Service firms show labor, procurement, data, or customer trust. Food and agriculture suppliers show traceability, safety, packaging, and water. Logistics firms show fuel, driver welfare, maintenance, and route planning. The same model can hold across sectors, but the material issue changes.

Future empirical work should also test whether staged evidence improves buyer confidence or finance access. That would move the research from applied model to validated tool. For the present paper, the methodological claim stays narrower: the model is coherent, source-based, and usable for managerial diagnosis.

3.6 Trustworthiness, Boundaries, and Ethics

Trustworthiness rests on transparent reasoning, source discipline, and internal consistency. The paper does not present illustrations as field data. It does not claim predictive accuracy. It does not invent firm results. Its model is diagnostic and practical.

Ethically, the paper refuses two weak positions. One position excuses constrained firms because they lack capacity. The other judges them by systems built for larger firms. Both positions fail. The paper instead demands credible progress on material issues and honest communication about capacity.

Method limits are acknowledged. The paper does not measure environmental impact, social outcomes, or financial performance in real firms. Later research can apply the model across sectors and test whether stronger scores relate to cost reduction, buyer retention, safety, compliance, or finance access. The analysis prepares that work by giving the test a coherent shape.

Chapter 4: Model and Analysis

4.1 Model Overview

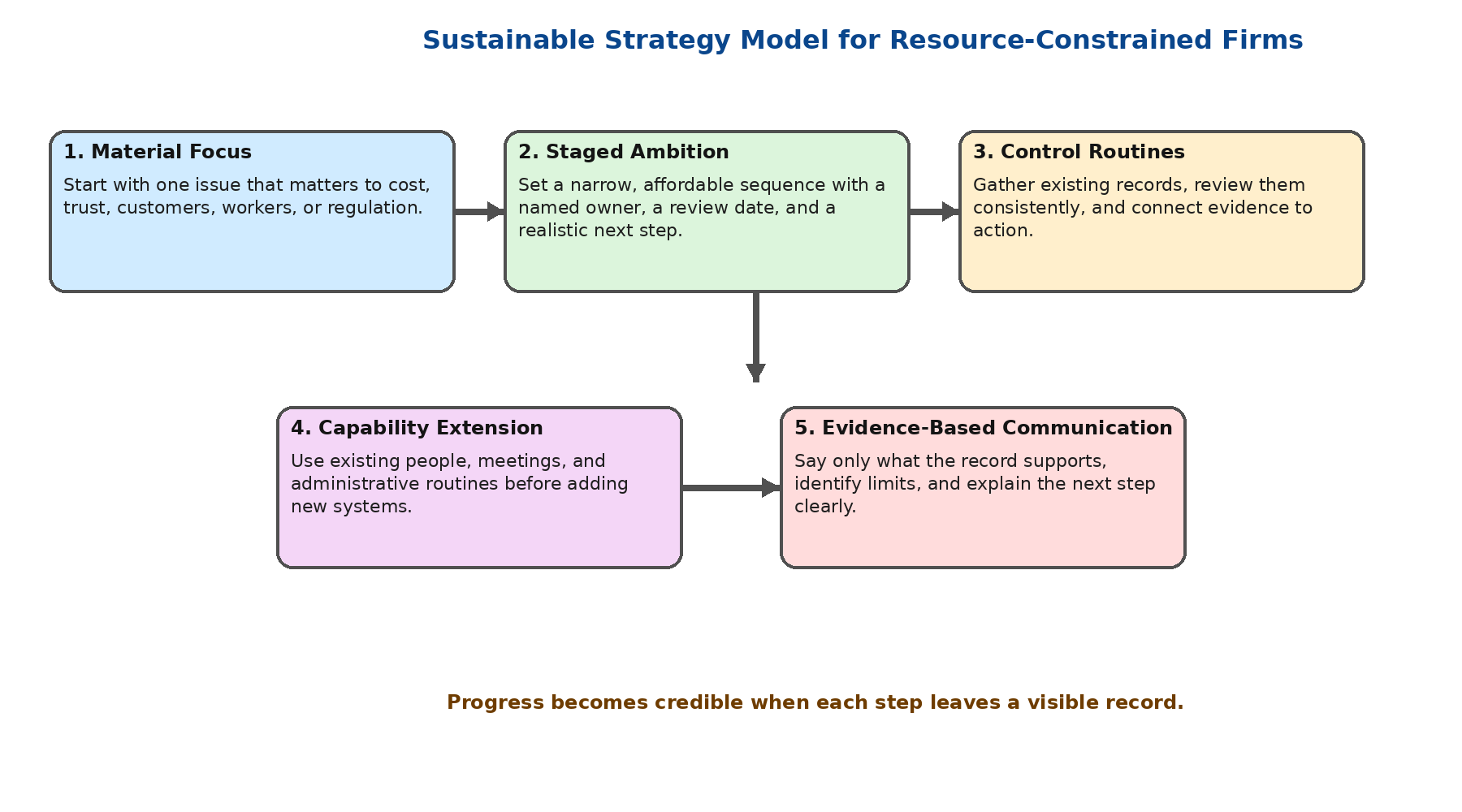

At the center of the model is a simple premise: a resource-constrained firm should begin by asking what material exposure it is actually managing. That question shifts attention away from appearance and toward evidence. The firm has to identify the issue, select a manageable action, assign responsibility, keep the record, review progress, and speak within the evidence.

The model uses five disciplines. Material focus selects the issue. Staged ambition limits the starting action to what the firm can manage. Control routines turn action into evidence. Capability extension uses existing people, records, and habits. Evidence-based communication protects the firm from claims it cannot defend.

Order matters. A firm that begins with a public statement invites overclaiming. A firm that begins with exposure and evidence builds a stronger position. The model rewards the most defensible record rather than the largest promise.

Figure 1. Five-discipline model for sustainable strategy under constraint.

4.2 Variable Operationalization

Material focus is strong when the chosen issue is connected to cost, risk, buyers, workers, regulation, or trust. It is weak when the issue is selected because it sounds attractive. Evidence for material focus includes buyer requests, cost data, incident logs, supplier risks, and management notes.

Staged ambition is strong when the action has a defined owner, cost, schedule, and review point. It is weak when the firm announces a broad target without resources. Evidence includes action plans, budget notes, training records, and review dates.

Control routines are strong when data are recorded, reviewed, and used for decisions. They are weak when records exist in fragments. Evidence includes logs, meeting notes, exception reports, supplier files, maintenance sheets, and corrective actions.

Capability extension is strong when the firm adapts existing routines rather than waiting for a new department. It is weak when leaders postpone action until a perfect system exists. Evidence includes supervisor roles, finance files, procurement checks, and training routines.

Evidence-based communication is strong when claims match the record. It is weak when public language runs ahead of proof. Evidence includes claim-review notes, completed action records, and written limits.

Table 3. Diagnostic scoring guide for the sustainable strategy model

| Variable | Weak practice | Stronger practice | Evidence |

| Material focus | Issue chosen because it sounds attractive. | Issue tied to cost, risk, buyer demand, labor, regulation, or trust. | Risk note, buyer request, cost record, incident log. |

| Staged ambition | Broad promise without money, owner, or sequence. | Narrow action linked to present capacity and next support need. | Action plan, budget note, review date. |

| Control routines | Data collected unevenly or not reviewed. | Record kept by a named owner and reviewed on schedule. | Log, minutes, exception report. |

| Capability extension | Firm waits for a new system before acting. | Existing routines are adapted for evidence and review. | Maintenance, procurement, training, or finance file. |

| Evidence-based communication | Claims exceed what the firm can prove. | Communication states completed work, limits, and next step. | Claim review, evidence file, signed note. |

4.3 Illustrative Scenario

Consider a small manufacturing supplier facing buyer renewal pressure. The buyer asks for proof on waste handling, labor training, and energy use. The supplier has fifty workers, a production supervisor, one accounts officer, and an owner-manager responsible for customers. Records exist, but they are scattered. Waste appears in production notes. Energy appears in bills. Training appears in supervisor memory and occasional sheets. Supplier documents sit in email folders and invoices.

In the illustrative manufacturing case, waste and energy emerge as the most immediate material issues because they touch operating cost, buyer scrutiny, and day-to-day production discipline. The most sensible starting move is therefore modest: assemble a waste-and-energy evidence file, confirm who owns the record, and pair that record with a basic training check.

A qualitative reading of the case shows where strength and fragility coexist. Material focus is well chosen because the issue is real and visible. Ambition remains manageable when improvement is staged rather than announced broadly. The weak point lies in scattered records, which means control routines need consolidation before any public-facing claim should be made. Existing staff roles nevertheless offer enough capacity to support early implementation if responsibilities are kept clear.

Read this way, the case yields a practical sequence rather than a numerical result: define the issue, gather the record, review the record inside ordinary management, correct obvious gaps, and communicate only what can be defended. That sequence matters because it converts responsible intention into a repeatable operating habit.

4.4 Qualitative Reading of the Model

The model is best understood through qualitative aids rather than through score-based reading. The tables in the analysis explain strategic pressures, literature lessons, variable contrasts, and implementation tasks. The figures added below show how the model fits together visually and how a constrained firm can move from problem recognition to disciplined action.

Each aid is placed close to the discussion it supports. Tables remain descriptive and practice-oriented, while figures stress sequence, governance, and the relationship among ownership, evidence, review, and communication.

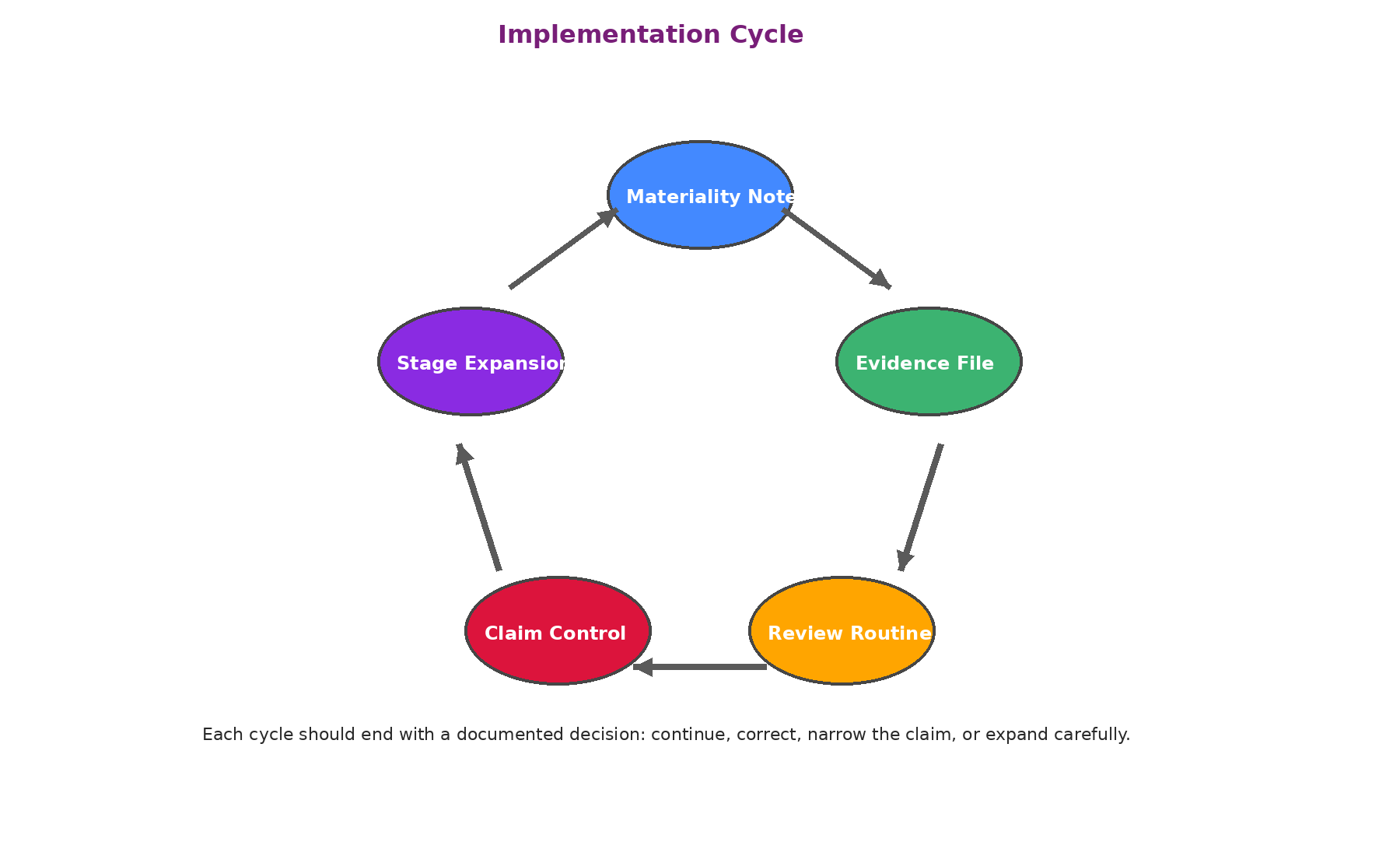

4.5 Implementation Sequence

Implementation begins with a one-page materiality note. The note names the issue, states why it matters, identifies the owner, lists the available record, and sets a review date. This document is small by design. A constrained firm does not need a long policy before it begins. It needs a usable management note that directs attention.

After the note, the firm builds an evidence file. The file can be digital or physical. Its value lies in order rather than sophistication. Waste tickets, energy bills, training records, supplier checks, and review notes belong in one place. A file that staff can update and management can review is stronger than a reporting template nobody uses.

Review then turns evidence into strategy. The firm should ask what the record shows, what action is required, what cost is attached, and what can be communicated. This review should happen inside an existing meeting rather than as an extra ceremonial event. Operations, finance, procurement, and customer meetings already hold the issues sustainability needs to address.

Figure 2. Implementation cycle from issue selection to staged expansion.

Implementation ends each cycle with a claim decision. The firm decides what it can say, what it cannot say, and what it needs to do next. This final step protects the firm from overclaiming. It also gives buyers and lenders a clearer account of progress.

4.6 Risk Register and Safeguards

Several risks appear during implementation. Overcommitment appears when leaders promise more than the firm can support. Indicator overload appears when the firm tracks more data than it can review. Record fragility appears when one person holds the evidence informally. Buyer pressure appears when the supplier agrees to demands before capacity is clear. Communication risk appears when public language outruns proof.

Each risk needs a safeguard. Overcommitment requires staged ambition. Indicator overload requires fewer metrics tied to material issues. Record fragility requires an evidence file and a named backup. Buyer pressure requires negotiated stages and written support needs. Communication risk requires claim review before release.

The safeguard logic keeps the model practical. A firm does not need to eliminate every risk before acting. It needs to know which risk threatens credibility and how to contain it. This keeps implementation active without encouraging reckless claims.

Risk review also supports learning. A weak cycle does not call for cosmetic repair; it calls for a better decision. If records are thin, management gathers and reviews them more consistently. If ownership is vague, responsibility is narrowed and assigned more clearly. If ambition is too broad, the firm reduces the claim and tightens the next step. The model becomes useful when it changes the next management decision.

4.7 Implementation Pathway

The implementation pathway has six movements. The firm identifies the material issue, writes a one-page materiality note, assigns an owner, creates the evidence file, holds a review, and approves only the claim supported by the record. Every movement has a management purpose. The issue focuses attention. The note prevents drift. The owner creates accountability. The file preserves evidence. The review turns records into decisions. The claim decision protects credibility.

This pathway works because it is small enough to fit into constrained firms. It does not require a new unit, expensive software, or external assurance at the start. It requires a disciplined owner and a review habit. That is a realistic base for firms that cannot stop operations to build a full reporting system.

Implementation should also include a backup owner. Small firms often depend on one person for operational memory. If that person leaves, the evidence trail collapses. A backup owner protects continuity. It also signals that sustainability is a firm routine, not the private effort of one employee.

The pathway becomes stronger when tied to buyer or lender communication. A firm can show the materiality note, evidence file, review date, and next action. This gives external actors a document trail they can assess. It also keeps the firm from speaking beyond proof.

4.8 Model Stress Tests

The model should withstand pressure rather than work only under tidy conditions. A buyer can request evidence quickly, a lender can ask for risk documentation, or a customer can challenge a public claim before the firm has a mature reporting system. Under that pressure, the safest response is not imitation of a larger company. It is disciplined proof: name the issue, show the record, identify the owner, state the next review date, and avoid claims that outrun evidence.

A record weakness gives the model its clearest test. A small firm can know that waste was reduced, training occurred, or supplier checks were made, yet still lack a stable evidence trail. The model does not allow the firm to rely on memory. It directs the firm to begin the record from a known date, assign ownership, and state the limit plainly. The responsible claim is not that a long history exists. The responsible claim is that a controlled routine has begun.

Finance pressure creates another test. A firm can identify the machine, process, or supplier practice causing waste, but lack the capital needed for immediate correction. The model separates low-cost evidence work from higher-cost improvement. The firm can document the exposure, show the current routine, estimate the support needed, and use that evidence in conversation with buyers, lenders, or advisers. Staged ambition protects credibility because it does not pretend that capacity already exists.

Staff turnover also tests the model. In resource-constrained firms, operational knowledge often sits with one experienced employee. When that person leaves, the evidence can disappear with them. The model responds by requiring a file, a backup owner, and a review routine. Responsibility becomes part of the firm rather than the private memory of one worker.

The stress tests confirm the paper’s central management position: sustainable strategy under constraint is credible only when exposure moves into evidence, evidence moves into review, and review governs the claim. A weak test result is not a failure of the model. It shows the next management action.

Chapter 5: Discussion

5.1 Interpretation of Findings

The model shifts the starting question from reputation to control. A constrained firm does not gain credibility by sounding like a larger organization. It gains credibility by proving that it manages one material exposure responsibly. This position changes how sustainability should be read in small-firm settings.

Ambition becomes credible when it is staged. A broad sustainability statement without records carries little value. A narrow action with a clear owner, file, review date, and evidence trail carries more value because it survives questioning. This is the paper’s main managerial claim.

The model also reframes support. Buyers, lenders, and advisers should not ask constrained firms for imitation. They should ask for evidence aligned with stage. A buyer can request a materiality note, evidence file, review schedule, and next action. A lender can ask which finance need blocks improvement. An adviser can help convert existing records into usable evidence.

Communication enters the discussion as a form of risk control. A constrained firm should not communicate to appear advanced. It should communicate to state what it has done, what record supports the claim, and what remains outside current capacity. This protects trust.

5.2 Avoiding Overclaiming

Overclaiming often begins when external pressure outruns internal evidence. A firm wants to satisfy a buyer, secure finance, or appear modern. Language expands before practice catches up. That is the point where sustainability becomes unsafe. Even real effort loses credibility when attached to claims the firm cannot prove.

The model handles this risk by making communication the final discipline. A claim follows issue selection, staged action, record building, review, and ownership. This order gives the firm a stronger voice. It also gives the firm a legitimate reason to state limits.

In a constrained firm, restraint reads as professional control rather than weakness. A statement such as “the firm has begun recording packaging waste and will review three months of data before setting a reduction target” is more credible than a broad claim of environmental leadership with no record. The smaller statement carries more authority because it can be checked.

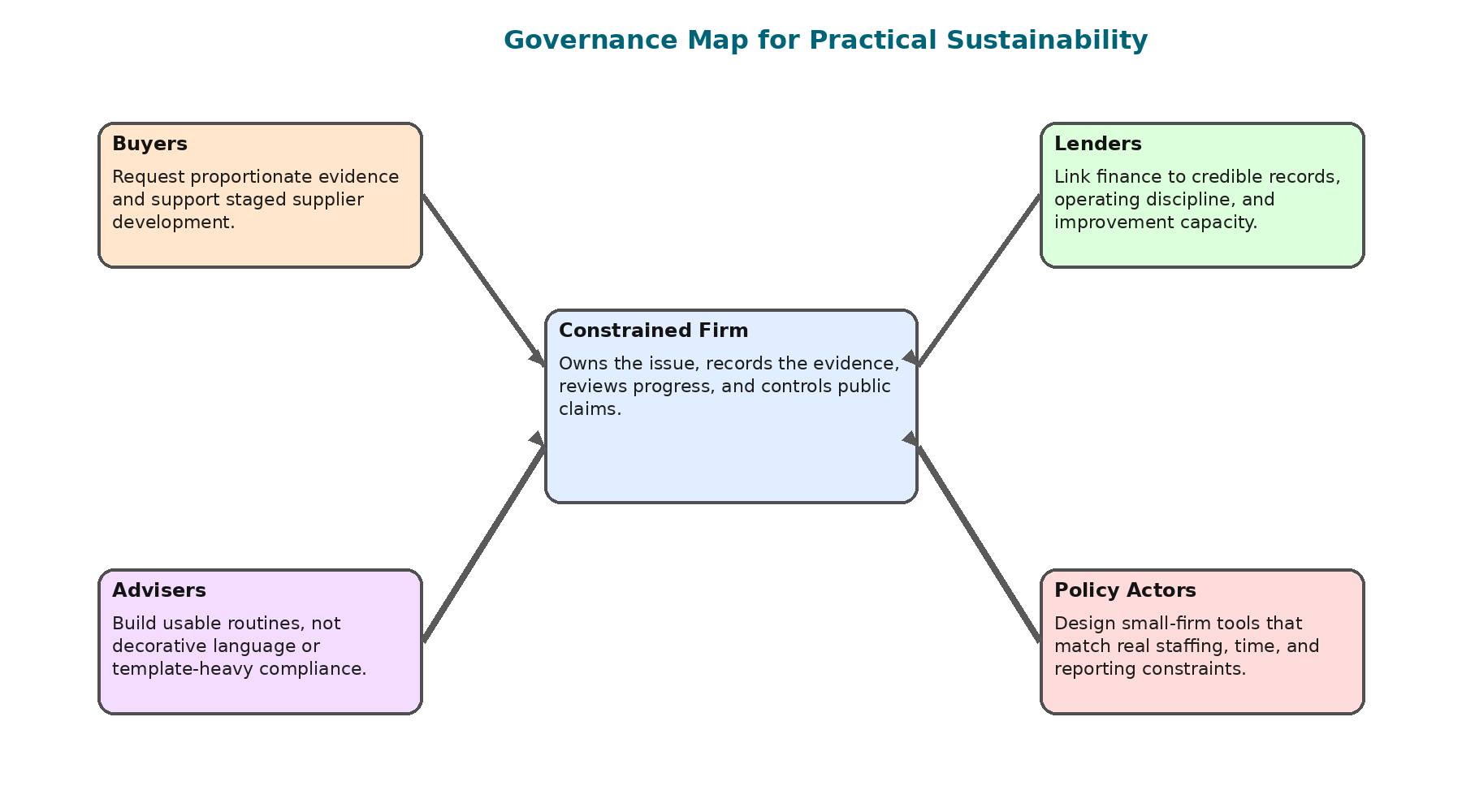

5.3 Institutional Implications

Responsibility is shared across the supply chain. A supplier has to act, but buyers shape the terms of action. Demanding evidence without time, guidance, or support produces defensive paperwork. Requesting staged evidence tied to material issues produces better practice.

Lenders also have a role. If sustainability reduces risk, finance should support the improvements that reduce that risk. Metering, training, safer equipment, waste handling, and basic record systems all require cost. A lender that asks for risk evidence without considering finance leaves the firm trapped between demand and capacity.

Policy actors can support smaller firms through simple templates, training, and staged standards. Complex reporting demands often produce compliance theatre. A simple materiality note, record file, owner designation, and review schedule can produce stronger discipline.

5.4 Managerial Consequences

Managers gain a sharper discipline from the model. Instead of treating sustainability as a separate topic, they place it inside existing work. Waste enters production review. Energy enters finance and maintenance review. Labor practice enters supervision and training. Supplier evidence enters procurement. Communication enters claim approval. Sustainability becomes a management question, not a parallel speech.

This shift changes accountability. The owner-manager no longer carries the issue alone. The production supervisor, accounts officer, procurement worker, and adviser each hold part of the record. That distribution matters because it turns sustainability from personality-driven effort into organizational routine.

Managerial time is still limited. The model respects that limit by narrowing the starting issue. A firm that tries to address everything creates fatigue. A firm that selects one material issue, builds evidence, and reviews it repeatedly builds capacity. The disciplined small start is stronger than the broad unreviewed agenda.

The model also improves conversation with external actors. A manager can tell a buyer: this is the issue, this is the record, this is the action, this is the support needed. That answer is harder to dismiss than a vague statement of commitment.

5.5 Consequences for Buyers and Lenders

Buyers gain a more useful assessment tool. Instead of judging suppliers by the appearance of a sustainability document, they can assess materiality, ownership, record quality, review routine, and claim restraint. This creates a stronger basis for supplier development. It also reduces the temptation for suppliers to copy language from larger firms.

Lenders gain a clearer link between sustainability and risk. A firm with energy records, safety logs, supplier checks, and review notes is easier to assess than a firm with broad claims and no evidence. Finance can then be tied to specific improvements: equipment, metering, training, storage, or record systems. Sustainability becomes part of credit reasoning rather than a separate virtue statement.

Both buyers and lenders also gain insight into capacity gaps. A supplier that lacks a record system needs a different intervention from a supplier that has records but no review. A firm with a finance bottleneck needs capital, not another form. This distinction improves institutional support.

External actors should therefore reward evidence discipline. The reward does not need to be symbolic. It can appear as preferred-supplier status, staged compliance timelines, better access to finance, or advisory support. Such incentives make credible practice more attractive than exaggerated language.

5.6 Sector Variations

Sector differences change the material issue but not the discipline. A small manufacturer begins with energy, scrap, machine downtime, training, or waste handling. A logistics firm begins with fuel, vehicle maintenance, driver welfare, and route discipline. A service firm begins with labor practice, procurement, data protection, and customer trust. A food supplier begins with traceability, water, packaging, safety, and spoilage.

The model works across sectors because it asks the same questions. What issue matters most? What action fits current capacity? Who owns the record? Where does evidence sit? What claim survives review? These questions retain force even when the sector changes.

Sector variation also shows why generic ESG checklists fail smaller firms. A checklist can ask every firm the same question. Strategy cannot. Strategy has to read exposure. The supplier handling food traceability has a different material issue from the service firm managing labor turnover. Standardized reporting has value, but strategy starts with firm-specific exposure.

Advisers should therefore avoid universal templates as the primary tool. Templates help only after materiality is known. The stronger advisory sequence is diagnosis, materiality note, evidence file, review routine, and claim control. That order respects sector difference while keeping a common discipline.

5.7 Contribution to Applied Strategy Research

Applied strategy research gains from a model that treats constraint as an operating condition rather than a background detail. Smaller firms do not simply lack resources; they face specific combinations of buyer dependence, finance pressure, thin staffing, weak records, and legitimacy exposure. Those conditions change what credible strategy requires.

The model contributes by naming the points where sustainability becomes real: issue selection, staged action, ownership, evidence, review, and claim control. Each point can be observed. Each point can fail. Each point can be improved. This makes the model useful to managers and assessors.

Management control receives special attention because evidence is where responsibility becomes testable. A firm that records, reviews, and acts on a material issue has moved beyond language. A firm that communicates within its record has reduced greenwashing exposure. This is the paper’s main applied contribution.

The research also shows that external actors shape implementation. Buyers, lenders, advisers, and policy actors do not stand outside the firm’s sustainability practice. Their demands, timelines, finance decisions, and support tools influence what constrained firms can prove.

Chapter 6: Conclusion and Recommendations

6.1 Summary of Findings

The study finds that sustainable strategy in resource-constrained firms begins with evidence rather than image. Smaller firms encounter buyer, lender, customer, regulatory, and community pressure before they possess formal sustainability systems. This does not remove their responsibility. It changes the way responsibility has to be organized.

The strongest finding is the need for sequence. A constrained firm cannot begin with a broad claim. It has to begin with a material issue, a staged action, an evidence file, a named owner, a review routine, and controlled communication. When those elements are present, early-stage sustainability practice becomes credible.

Materiality emerges as the entry point. A firm gains focus by selecting the issue tied most directly to cost, risk, buyers, labor, regulation, or trust. Staged ambition then prevents overreach. Control routines convert action into evidence. Capability extension uses existing people and records. Evidence-based communication protects the firm from overclaiming.

The model also shows that responsibility is shared across institutional relationships. Managers must act, but buyers, lenders, advisers, and policy actors shape what action becomes realistic. Pressure without support produces paperwork. Pressure joined to evidence discipline produces better practice.

6.2 Recommendations for Managers

Managers should begin with a one-page materiality note. The note should state the issue, explain why it matters, name the owner, identify the record, and set the review date. This document should be short, specific, and usable. A long policy that nobody reviews has little value in a constrained firm.

Managers should keep the starting action narrow. One material issue, one owner, and one evidence file give the firm a defensible base. Once that routine works, expansion becomes safer. Moving too quickly across several issues weakens ownership and record quality.

Managers should build evidence from existing records. Energy bills, training sheets, waste tickets, supplier invoices, maintenance notes, and incident logs already contain useful data. The task is to gather them, review them, and connect them to action.

Communication should be controlled through a claim-review step. A statement should be released only when a record supports it. The firm should state completed action, evidence held, limits, and the next step. This protects credibility and reduces exposure.

6.3 Recommendations for Buyers and Lenders

Buyers should replace broad supplier demands with staged evidence requests. A supplier should be asked to identify its material issue, show the record, name the owner, and state the next review date. This is stricter than accepting a copied sustainability statement because it tests practice.

Buyers should also recognize capacity gaps. A supplier that lacks a record file needs support different from a supplier that has records but no review routine. Templates, reasonable timelines, training, and staged requirements improve evidence quality.

Lenders should treat sustainability as part of risk assessment. Energy waste, safety weakness, supplier exposure, and poor records all affect operating risk. A firm that shows disciplined records and staged action gives the lender better information.

Finance should connect to practical improvements. Metering, equipment repair, training, safer storage, and record systems improve both sustainability and repayment confidence. A lender that asks for risk control should consider the capital needed to produce it.

6.4 Recommendations for Advisers and Policy Actors

Advisers should stop writing large sustainability statements before evidence exists. Their work should begin with materiality, records, ownership, and review. The best adviser helps the firm become more auditable, not more decorative.

Figure 3. Governance map linking the constrained firm with external actors.

Training should focus on evidence habits. Staff need to know what is being recorded, who receives the record, and what decision follows. Awareness without record discipline does not change the firm.

Policy actors should design smaller-firm tools that fit real capacity. A simple materiality note, record-file template, review form, and claim-control checklist can create stronger discipline than a long reporting form.

Sector bodies can support shared templates for common exposures. Manufacturing firms need waste and energy tools. Logistics firms need fuel, maintenance, and driver welfare tools. Food suppliers need traceability, safety, packaging, and spoilage tools. Service firms need labor, procurement, and customer-trust tools.

6.5 Implementation Roadmap

Implementation should follow a five-step path. The firm selects one material issue. It writes a short note explaining why the issue matters. It assigns ownership. It creates the evidence file. It reviews the file and approves only claims supported by records.

The starting cycle should run for a defined period, such as three months. That period gives the firm enough evidence to see pattern without creating a heavy reporting burden. At the review point, management decides whether to continue, adjust, or expand.

The roadmap should be tied to existing meetings. Production review, finance review, procurement review, and customer review already hold sustainability-relevant decisions. Adding the material issue to those meetings makes responsibility part of management rather than a separate performance.

Expansion should follow evidence. A firm that has stabilized one issue can add another. A firm that has not stabilized the first issue should strengthen the record before widening the agenda.

Table 4. Implementation roadmap for resource-constrained firms

| Step | Managerial task | Evidence produced |

| Materiality note | Name the issue and explain why it matters to cost, risk, buyers, labor, regulation, or trust. | One-page note with owner and review date. |

| Evidence file | Collect existing records and identify gaps. | Waste tickets, energy bills, training sheets, supplier checks. |

| Review routine | Place the record inside an existing meeting. | Minutes, action note, exception review. |

| Claim control | Approve only statements supported by records. | Claim-review note and supporting file. |

| Stage expansion | Add the next material issue after the starting routine works. | Updated plan, new owner, next record file. |

6.6 Limitations and Future Research

The paper remains conceptual and applied. It does not claim statistical validation or predictive certainty. Its contribution lies in disciplined synthesis, a usable managerial model, and practical illustrations that show how smaller firms can turn responsibility pressure into workable routines without overstating what the evidence can support.

Future research should test the model in real firms. Interview studies can show how managers receive sustainability demands and where implementation breaks down. Document reviews can test whether evidence files exist. Buyer and lender interviews can show which records influence trust and finance decisions.

Sector comparison would deepen the model. Manufacturing, logistics, food supply, service, and trading firms face different material issues. The five-discipline model should hold across sectors, but the evidence types and starting issues differ.

Future work should also test whether stronger evidence routines improve buyer retention, loan assessment, compliance readiness, or operating cost. That research would move the model from applied synthesis to empirical validation.

6.7 Monitoring Indicators for Constrained Firms

Monitoring should remain small enough to survive routine pressure. A constrained firm does not need a large dashboard at the start. It needs a short set of indicators tied to the material issue. Waste weight, energy cost, training completion, incident frequency, supplier-file completion, customer complaint trends, and corrective-action closure all serve as practical indicators when they connect to the selected issue.

An indicator becomes useful only when management reads it. A figure kept in a file without review does not improve strategy. The firm should record the indicator, compare it with the previous period, discuss the reason for change, and assign any needed action. The review note matters because it shows that the firm used the record rather than stored it.

Indicators should also be limited by capacity. A firm that tracks ten measures without review weakens its own system. A firm that tracks two material measures and acts on them builds credibility. The test is not the number of metrics. The test is whether each metric informs a decision.

Good indicators also protect communication. When a firm knows exactly what it recorded, overclaiming becomes easier to avoid. The firm can state the evidence plainly: the period covered, the measure used, the change observed, and the next action. That style of communication is concrete enough for buyers and cautious enough for the firm.

6.8 Governance of Responsibility Inside the Firm

Governance in a constrained firm is not limited to boards or formal committees. It appears in ownership, escalation, review, and accountability. Someone has to keep the record. Someone has to review it. Someone has to approve claims. Someone has to decide when a risk needs money, training, or buyer negotiation. Without those roles, sustainability remains a loose intention.

Owner-managers need a light but firm governance system. A production supervisor can own waste records. An accounts officer can support energy evidence. A procurement worker can maintain supplier files. A senior manager can approve external claims. These roles do not require a new hierarchy. They require explicit assignment.

Escalation is also part of governance. A supervisor who finds repeated waste needs a path to raise the issue. An accounts officer who sees rising energy cost needs a review point. A procurement worker who sees supplier weakness needs permission to flag risk. Sustainability becomes stronger when staff know where evidence travels.

Governance also reduces dependence on personality. Many smaller firms rely on one trusted worker who knows the process. That person becomes the hidden evidence system. The firm gains stability when that knowledge is written down, shared, and reviewed. A record file, backup owner, and review routine convert individual memory into organizational capacity.

6.9 Practical Value of the Model

The practical value of the model lies in its ability to reduce confusion. Managers often face sustainability pressure as a cluster of demands. The model turns that cluster into a sequence. Select the material issue. Stage the action. Build the record. Use existing capability. Speak only where evidence exists. The sequence does not remove pressure, but it makes pressure manageable.

The model also helps external actors ask better questions. A buyer can ask for evidence rather than performance language. A lender can ask whether the requested finance improves a material risk. An adviser can ask which record already exists and how it should be reviewed. These questions are sharper than generic interest in sustainability.

The model supports fairness without weakening responsibility. It does not allow a firm to hide behind constraint. It also does not treat corporate imitation as the only proof of seriousness. The firm has to show progress on a material issue, and the progress has to be visible in records and review. That standard is fair precisely because it is demanding and realistic at the same time.

Practical value also appears in repeatability. Once a firm has learned to manage one issue through the sequence, it has a method for the next issue. The model becomes a learning device. Each cycle strengthens the firm’s ability to deal with buyers, lenders, regulators, workers, and customers.

6.10 Final Research Position

The final position of the study is that sustainable strategy under constraint is a matter of disciplined proof. A resource-constrained firm does not need to sound large. It needs to show that it manages a real issue responsibly. Evidence gives that claim force.

The paper’s central contribution is therefore practical and analytical. It gives constrained firms a route into sustainability without lowering standards. It gives external actors a way to judge progress without forcing imitation. It gives advisers a way to build records rather than rhetoric. It gives researchers a sharper account of how capacity, control, legitimacy, and communication interact inside smaller firms.

Responsibility under constraint is not a softer kind of responsibility; in some respects it is harder, because the firm has fewer buffers to absorb a mistake. Errors in claim, record, finance, or buyer communication carry immediate consequences. The model responds by placing restraint at the center of practice. The firm acts, records, reviews, and speaks carefully.

That is where the paper closes. Sustainable strategy becomes credible when a firm can point to the material issue it chose, the evidence it keeps, the person who owns the record, the review that governs action, and the claim the record supports. Anything beyond that remains aspiration. The standard defended here is proof.

6.11 Managerial Case Extension

Consider the manufacturing supplier again after six months of using the model. The firm now has a waste file, energy records, a training sheet, and a monthly review note. None of these records is elaborate. Together, they change the firm’s position. The owner-manager can now show the buyer what issue was selected, how evidence was kept, and what decision followed from review.

The records also reveal practical learning. Waste is higher on one production line after rush orders. Energy cost rises after machine stoppages. Training records show uneven onboarding when temporary workers enter the line. These observations do not require complex analytics. They require disciplined attention. The firm sees what it previously knew only informally.

The next stage becomes clearer. The firm can reduce packaging waste on the rush-order line, create a short onboarding sheet for temporary workers, and request finance for maintenance improvement. These actions are not separate from sustainability. They are sustainability expressed as cost control, labor discipline, process reliability, and buyer confidence.

The case extension shows why early evidence matters. Without records the firm speaks from memory, whereas with records it speaks from management. That shift is the difference between aspiration and credible strategy.

6.12 Stakeholder Trust and Operating Resilience

Stakeholder trust is built through repeated proof. A buyer trusts a supplier more when the supplier can show records rather than broad claims. Workers trust management more when safety and training records lead to visible action. Lenders trust the firm more when risk is named and connected to finance needs. Communities trust the firm more when environmental issues are acknowledged and managed.

Operating resilience grows from the same discipline. A firm that records waste understands process weakness. A firm that reviews energy cost sees exposure earlier. A firm that keeps training records reduces dependence on memory. A firm that controls claims reduces reputational risk. These gains do not appear as a single transformation. They appear as better management.

Resilience also protects the firm during disruption. When a buyer audit arrives, evidence is ready. When a worker leaves, the record remains. When a lender asks about risk, the firm has a practical answer. When cost rises, management can look at records instead of guessing. The firm becomes less fragile because knowledge is no longer trapped in scattered memory.

Trust and resilience therefore become linked. The same routines that help the firm prove responsibility also help it manage operations. This connection is central to the paper’s argument. Sustainability is strongest in constrained firms when it improves the quality of management itself.

6.13 Decision Rules for Responsible Expansion

Expansion should follow decision rules. A firm should not add a new sustainability issue until the current issue has an owner, a record, a review routine, and a claim standard. If any of those elements is missing, expansion spreads weakness. If all are present, expansion builds capacity.

The next issue should be selected through materiality, not preference. A firm should ask which exposure now carries the strongest connection to cost, risk, buyers, labor, regulation, or trust. The answer directs the next cycle. This keeps the firm from following fashionable language or external pressure without analysis.

Expansion also requires a capacity check. The firm should ask what the next issue costs in time, money, skill, and evidence. If the cost is too high, the firm should identify support needs rather than pretend capacity exists. This preserves credibility and gives buyers, lenders, and advisers a concrete place to help.

Responsible expansion is therefore neither slow nor fast by habit. It is evidence-paced. The firm widens the work when records and routines justify the next move. That standard protects both ambition and truth.

6.14 Evaluation Criteria for Practice

Evaluation should focus on what the firm can prove. A useful review asks whether the material issue is named, whether the evidence file exists, whether the owner is active, whether the review produced action, and whether communication stayed within the record. These criteria are simple, but they cut through weak sustainability language.